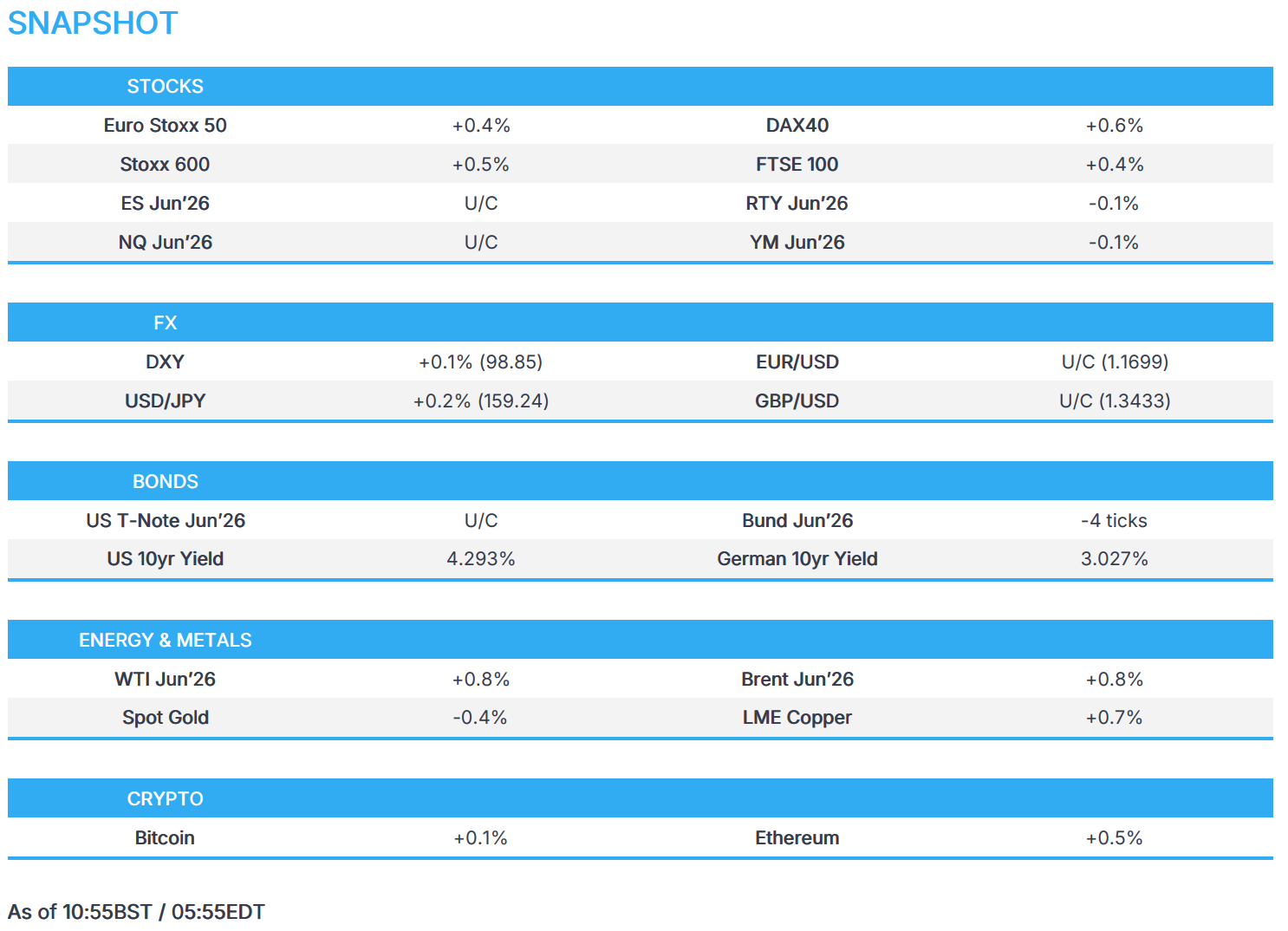

US Market Open: DXY and crude tentative into US-Iran weekend talks, US inflation data ahead

10 Apr 2026, 11:30 by Newsquawk Desk

- US President Trump posted "Iran is doing a very poor job, dishonourable some would say, of allowing Oil to go through the Strait of Hormuz. That is not the agreement we have!"

- Iran reiterated that no talks will happen until attacks stop and no delegation is heading to Pakistan, despite the expectation of talks to take place on Saturday. Further, an informed source stated Tehran rules out the option of negotiating with Washington until a complete ceasefire is established in Lebanon, and has strongly asserted this position.

- Ukrainian President Zelensky's top aide/negotiator Budanov reportedly sees Ukraine nearing a deal with Russian President Putin, Bloomberg reported.

- Crude edges higher heading into high-stakes US-Iran talks on Saturday.

- European bourses set for a third consecutive weekly gain, SW FP plummets following weak guidance; US equity futures flat.

- DXY muted, EUR and HUF look to Hungarian election.

- Fixed benchmarks tread water heading into US CPI and US-Iran peace talks.

- Looking ahead, highlights include Canadian Jobs Report (Mar), US Inflation (Mar), University of Michigan Consumer Sentiment Prelim. (Apr), Credit Ratings updates including Moody's on France, S&P on the UK & Scope Ratings on Hungary.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.5%) are gaining heading into the US-Iran talks at the weekend. If indices can hold onto their gains, it would be the first Friday since the Iran war began that stocks would end in the green. The complex has been fairly choppy this morning, with some pressure seen alongside a slight bid in the crude complex, but then reversed those losses after reports suggested that Ukraine’s top aide Budanov reportedly saw Ukraine nearing a deal with Russian President Putin.

- European sectors are broadly in the green. Media, Health Care and Technology tops the sector pile while Basic Resources and Travel and Leisure lags. The tech sector has been given a boost after TSMC reported YTD sales that beat estimates, supporting the likes of ASML and STMicroelectronics. On the other hand, Travel and Leisure is under pressure following earnings by Sodexo, in which the Co. cut its 2026 organic revenue growth forecast, citing ongoing execution challenges.

- US equity futures (ES/NQ U/C, RTY -0.1%) are posting modest losses ahead of the US CPI later, in which headline inflation is expected at 3.3% Y/Y, rising from 2.4% while core inflation also expected to rise to 2.7% Y/Y from 2.5%.

- TSMC (2330 TT) YTD (TWD): Sales 1.13tln (exp. 1.12tln, prev. 0.839tln Y/Y).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Energy prices continue to dominate price action across G10 currencies, with USD leading. Focus remains on geopolitical updates, none of which overnight did much to spur crude benchmarks ahead of US/Iran talks scheduled this weekend. This morning, newsflow has been light, though there were reports that Iran said no talks would happen until attacks [on Lebanon] stop. US CPI is due at 13:30 London time; today's release should not be a game-changer for the Fed unless the print significantly exceeds expectations, policy will likely be dictated after members assess the second round effects of the Middle East conflict in future months' prints.

- Do note that the USD saw some mild selling pressure to session lows of 98.79 (vs 99.00 peak), after reports suggested that Ukraine’s top aide Budanov reportedly saw Ukraine nearing a deal with Russian President Putin. But it is worth highlighting that the interview was conducted on April 4th, while recent rhetoric via Ukrainian President Zelensky suggested that Putin is not genuinely seeking peace.

- EUR will look to Sunday's Hungarian election (Full Preview), where polling suggests opposition support Tisza will take power, though still unclear whether the opposition will gain a supermajority or a simple majority. Desks suggest a supermajority sees HUF and EUR strength, while a simple majority may see initial HUF gains and potential EUR strength, "likely to be pared". EUR/USD marginally surpassed the 1.17 level with a session high at 1.1702. Elsewhere for the single currency, German inflation was left unrevised at 1.1% on a monthly basis.

- For NOK, Norwegian core inflation this morning surprised to the downside, but still remains elevated on a 3% handle, in line with the Norges Bank's forecast. With markets shrugging off the modest gains in crude this European morning, the net energy exporter's currency is flat/modestly lower against EUR within a 11.0839-11.1194 range.

- Kiwi is the worst-performing G10 currency against a stronger buck, after the rally in the pair stalled just above 0.5870. Likely an element of profit-taking after gains over the past two days, with markets continuing to price 75bps of hikes by year end, unchanged from Thursday's close. Additionally, key metals trade 1-2% lower - as such, AUD also underperforming against the greenback.

FIXED INCOME

- Fixed benchmarks are flat/mixed this morning, as the complex awaits US CPI later today and heading into the weekend, where US and Iranian officials are to meet for peace talks in Pakistan. While preparations are proceeding "full steam ahead" in the Pakistani capital, both sides have issued warnings that could still derail the meeting. Heading into the confab, US President Trump said he is optimistic that an Iran peace deal is within reach, but warned that if no deal is reached, “it is going to be very painful”.

- USTs are currently flat, with price action lacklustre heading into US CPI. Currently trades within a 111-05 to 111-11+ range, with the 2yr yield hovering near familiar levels at 3.795%, but still well off the extremes seen during the heights of the Iranian war. Traders are currently awaiting the US inflation report, where analysts expect consumer prices to rise by 0.9% M/M (prev. 0.3%), and the annual rate to jump to 3.3% Y/Y (prev. 2.4%); core inflation is expected to rise 0.3% M/M (prev. 0.2%). Officials say inflation remains too high, with upside risks if oil shocks spill into core prices and expectations, although expectations are still seen as well anchored at this point.

- Recapping the action this week, USTs are currently higher by 16 ticks vs the Monday open, with strength facilitated by ceasefire related optimism – however, US paper has pulled back from highs given the fragile nature of the two-week pause so far. US 2s10s is near enough unchanged since the start of the week, but did experience some steepening amidst the initial ceasefire related optimism.

- Bunds and Gilts are trading on either side of the unchanged mark, with both currently just off session lows. Earlier, Final German Inflation was unrevised in March, and had little impact on Bunds this morning. The action this week across Bunds is reflective of the easing tensions in the Middle East, with the 2yr yield now residing around 2.56% vs the Tuesday open at 2.65%. This has also been reflected in ECB pricing – with money markets fully pricing in an ECB rate hike in April towards the start of the week, now, only 6bps. The temporary ceasefire will allow policymakers to bide their time and assess whether second-round inflation effects filter through into the economy – markets still pricing in two hikes by year-end.

- Italy sold EUR 8.0bln vs exp. EUR 6.25-8.0bln 2.40% 2029, 3.30% 2033 and 3.95% 2041 BTP.

- Australia sold AUD 1bln 1.00% December 2030 bonds, b/c 3.29, avg. yield 4.6278%.

COMMODITIES

- Oil rose for a second consecutive session after Saudi Arabia said attacks on energy infrastructure had reduced its production capacity, with Brent climbing above USD 96/bbl. Despite the rebound, both benchmarks remain on course for their largest weekly loss since June, following Tuesday’s ceasefire announcement. Middle East situation aside, a piece in Bloomberg suggested that Ukraine’s top aide Budanov reportedly saw Ukraine nearing a deal with Russian President Putin – though this interview was conducted on April 4th. Nonetheless, this spurred some pressure in Brent Jun’26, falling to a session low of USD 96.03/bbl before paring back towards USD 97/bbl mark, with gains currently around USD 1/bbl.

- Ahead, the focus is on weekend talks between the US and Iran in Islamabad, Pakistan. The diplomatic picture remains complicated, however. US President Trump said he was "optimistic" about a deal but threatened Tehran over reported fees being levied on tankers in the Strait of Hormuz, adding that Iran was doing a "poor job" of allowing energy supplies to flow despite ceasefire commitments. He also asked Israeli PM Netanyahu to scale back attacks on Lebanon, amid concerns the fighting could undermine negotiations - a view echoed by both Iran and ceasefire mediator Pakistan, which have described Israel's Lebanon offensive as a truce violation.

- Spot gold trades subdued on either side USD 4,750/oz (USD 4,731-4,780/oz), but on track for a third straight weekly gain, supported by central bank buying and diplomatic hopes. Critical Metals’ CEO cautioned that bullion could face pressure if oil prices rebound materially, stoking inflation concerns and rate expectations.

- Copper is flat in indecisive trade with broader base metals mixed. 3M LME copper currently trades in a 12,641.00- 12,772.87/t range. In data, China’s factory deflation ended after more than three years, with PPI rising 0.5% Y/Y in March (exp. 0.4%), as surging energy costs snapped the deflationary streak.

- US offers 30mln barrels in crude oil exchange from the Strategic Petroleum Reserve, as part of IEA coordinate release.

- Japanese PM Takaichi said to release about 20 days of oil stockpiles in May.

- China allows state oil firms to release their reserves amid US-Iran conflict.

- TotalEnergies (TTE FP) said it shut down SATORP refinery in Saudi Arabia as safety precaution following processing train damage.

- EU and US nearing a critical minerals deal to "combat Chinese control", Bloomberg reported.

- Venezuela passes mining law as Acting President Rodriguez courts investment, according to Bloomberg.

TRADE/TARIFFS

- Taiwan is to launch an anti-dumping probe into China's polyamide films.

- Ecuador raises the duty on Colombian imports to 100% from 50%, citing Colombia's failure on border security.

NOTABLE EUROPEAN HEADLINES

- US President Trump endorses Hungarian PM Orban, reiterates that he's a truly strong and powerful leader with a proven track record delivering phenomenal results.

- UK retail footfall returned to growth in March as a number of visits to stores comprising of main street shops, retail parks and shopping centres for the five weeks to April 4th rose 2.4% Y/Y, according to the British Retail Consortium.

NOTABLE EUROPEAN DATA RECAP

- German Inflation Rate YoY Final (Mar) Y/Y 2.7% vs. Exp. 2.7% (Prev. 1.9%).

- German Inflation Rate MoM Final (Mar) M/M 1.1% vs. Exp. 1.1% (Prev. 0.2%).

- Norwegian Core Inflation Rate YoY (Mar) Y/Y 3.0% vs. Exp. 3.2% (Prev. 3%).

- Norwegian Core Inflation Rate MoM (Mar) M/M 0.1% (Prev. 0.7%).

- Norwegian Inflation Rate YoY (Mar) Y/Y 3.6% (Prev. 2.7%).

- Norwegian Inflation Rate MoM (Mar) M/M 0.2% (Prev. 0.6%).

- Italian Industrial Production YoY (Feb) Y/Y 0.5% (Prev. -0.6%).

- Italian Industrial Production MoM (Feb) M/M 0.1% vs. Exp. 0.5% (Prev. -0.6%).

- Swedish GDP MoM (Feb) M/M 0.0% (Prev. -1.1%).

CENTRAL BANKS

- US Senate Banking panel is no longer intending to conduct a confirmation hearing for Kevin Warsh next week with the delay due to paperwork.

- BoJ Deputy Governor Himino said no strict definition on what constitutes stagflation, adds must be vigilant to chance Middle East conflict, which if prolonged, could work to weigh on the economy and push up inflation. Doesn't think Japan's economy is in stagflation. Face dilemma if prolonged Middle East conflict pushes down growth and accelerates inflation. Will make appropriate decisions on price target and will make the appropriate decision at each meeting. Will take most appropriate policy to stably hit the inflation target, considering scale and duration of shocks and broader economic environment.

- BoK maintains the Base Rate at 2.50%, as expected.

- BoK said rate decision was unanimous and that Middle East conflict poses risks to growth. Growth likely to be below 2% this year. To thoroughly assess external and internal conditions including the Middle East situation. To closely monitor impact on inflation, growth and financial stability. Necessary to remain cautious about FX volatility. Inflation likely to be significantly above 2.2% this year. Raises 2026 GDP growth forecast to 2.0% from 1.8% and CPI forecast to 2.2% from 2.1%.

- BoK Governor Rhee said growth path to hinge on the Middle East and trade conditions, adds board members are in wait-and-see mode as Middle East conflict situation is too volatile. It is too early to judge the direction of the Middle East shock, stating that a temporary shock does not warrant a rate response, although a prolonged shock may require a policy response. Iran war has a bigger impact on inflation and growth outlook in South Korea than the war in Ukraine. To assess the size and duration of the Middle East war impact. Too early to discuss a rate hike amid Middle East volatility. Board needs to watch the course of Middle East negotiations first. Asian economies more vulnerable to supply-side impact from Iran war compared to European economies.

NOTABLE US HEADLINES

- Trump administration reportedly considering a new crackdown on Chinese telecom Carriers' US operations, according to the agency.

- US Treasury Secretary Bessent reportedly summoned Wall Street CEOs to discuss Anthropic's Mythos.

- BofA's weekly flow report noted USD 70.7bln into cash, USD 36.8bln into stocks, USD 8.7bln into bonds, USD 3.5bln into gold, USD 0.2bln into crypto.

GEOPOLITICS

MIDDLE EAST

- US President Trump posted "Iran is doing a very poor job, dishonourable some would say, of allowing Oil to go through the Strait of Hormuz. That is not the agreement we have!".

- US President Trump posted "There are reported that Iran is charging fees to tankers going through the Hormuz Strait — They better not be and, if they are, they better stop now!".

- US President Trump criticises WSJ for stating he declared premature victory in Iran, adds there is nothing premature about it, also said because of him, Iran will never have a nuclear weapon and oil will start flowing very quickly.

- Iran reiterates no talks will happen until attacks stop and no delegation is heading to Pakistan. However, it was reported that the Iranian delegation arrived in the Pakistani capital of Islamabad late on Thursday for upcoming talks, with the delegation led by Iranian Foreign Minister Araghchi and Parliament Speaker Ghalibaf.

- Informed source told Tasnim that news in some media about the arrival of Iranian negotiating teams to Islamabad to negotiate with Americans is completely false, adds until US fulfils commitments negotiations are suspended.

- Iranian delegation has not yet reached Islamabad despite plans for the first round of negotiations today, Pakistan media report.

- IRGC affirms Iran's armed forces have absolutely not carried out any launches towards any country during the ceasefire hours up to this moment.

- UK Government said UK PM Starmer and US Present Trump spoke this evening, and agreed there is a ceasefire in place, agreement to open the Strait, and we are at the next stage of finding a resolution. Discussed the need for a practical plan to get shipping moving again as quickly as possible and agreed to speak again soon.

- Iranian Supreme Leader Khamenei may deliver address to the nation soon, TASS reported.

- Israeli Chief of Staff Zamir said will continue the war in Lebanon, can return to the war against Iran at any moment and with greater force.

- Israel is working to continue the war on Lebanon within two days and 5 more days before responding to American pressures, Al Jazeera reported citing Ma'ariv sources.

- Israeli airstrike targets Habbouch town in southern Lebanon, while reported also noted that siren sound in Metula, Israel.

- Iranian media reported of intense activity of hostile drones in Iranian cities Tehran, Parachin, Tabriz, and other cities.

- Six rockets were fired from southern Lebanon towards Al Jalil in northern Israel.

- Air raid sirens have sounded in the Mizgav Am and Metula settlements in northern Israel.

- Air raid alarms were activated in Tel Aviv, while Israeli military said Hezbollah launched a missile at Israel which set off air raid alarms.

- Warning sirens sound in Kiryat Shimona and surrounding areas, according to Mehr News.

- Shipping traffic in Strait of Hormuz was down on Thursday as just six ships travelled through the strait with two oil tankers among the six ships, according to CBS.

RUSSIA-UKRAINE

- Ukrainian President Zelensky's top aide/negotiator Budanov reportedly sees Ukraine nearing a deal with Russian President Putin, Bloomberg reports; interview conducted on April 4th.

- Russia's Kremlin confirms envoy Dmitriev’s trip to the US, says Dmitriev is not negotiating on a Ukraine settlement.

OTHERS

- Chinese President Xi said China will never tolerate Taiwan independence, CCTV reported.

- North Korea's Foreign Minister tells Chinese counterpart that ties between the two countries are developing into an elevated new phase.

- China's Foreign Minister Wang Yi said it is China's steadfast stance to strengthen China-North Korea relations, irrespective of any shift in the international landscape, according to KCNA. North Korea has achieved results despite suppression by the US and Western powers.

- Cuba's President said asked the US to engage in a dialogue without condition and not demand changes from our political system.

CRYPTO

- Bitcoin tops USD 72k, while Ethereum briefly extends above USD 2.2k.

APAC TRADE

- APAC stocks were mostly higher following the gains on Wall Street, where markets extended on the ceasefire-driven momentum, although strikes continued in the region and Israel declared it will keep striking Lebanon ahead of talks next week. Furthermore, shipping through the Strait of Hormuz remained at a virtual standstill, and US President Trump criticised Iran on the Strait of Hormuz and warned it to stop charging tolls in the strait.

- ASX 200 was dragged lower by underperformance in tech and energy, while nearly all sectors were lacklustre, aside from the mild resilience seen in real estate and financials.

- Nikkei 225 rallied with index heavyweight Fast Retailing among the top gainers after its shares surged to fresh record highs following strong earnings results, while participants also reflected on PPI data, which ultimately printed mixed, but showed an acceleration for both the M/M and Y/Y figures.

- Hang Seng and Shanghai Comp were higher amid some strength in tech, property and auto stocks, while the latest inflation data for China was mixed as CPI printed softer-than-expected, but PPI slightly topped forecasts and showed a return to growth in factory gate prices for the first time in more than three years.

NOTABLE ASIA-PAC HEADLINES

- Japan's Finance Minister Katayama declines to comment on FX levels and said the government is prepared to take decisive action in markets, but will not elaborate on future potential measures. said: Speculation is intensifying in oil, futures, and currency markets.

- Japanese Finance Minister Katayama say unable to gauge the effect of a food sales tax reduction on prices at this stage and not in a position to discuss steps against possible oil supply deficits. Will co-chair a session on critical minerals on the margins of the G7 meeting. Private credit will be on the G7 agenda but no significant crisis is seen and Japan has no substantial exposure. G7 finance ministers unanimously agree the Middle East situation should not be extended.

- South Korean parties agree on an extra budget size of KRW 26.2tln, according to Yonhap.

NOTABLE APAC DATA RECAP

- Chinese Inflation Rate YoY (Mar) Y/Y 1.0% vs. Exp. 1.2% (Prev. 1.3%).

- Chinese Inflation Rate MoM (Mar) M/M -0.7% vs. Exp. -0.3% (Prev. 1%).

- Chinese PPI YoY (Mar) Y/Y 0.5% vs. Exp. 0.4% (Prev. -0.9%).

- Australian Private House Approvals MoM Final (Feb) M/M 0.2% vs. Exp. 0.2% (Prev. 1.1%).

- Australian Building Permits MoM Final (Feb) M/M 29.7% vs. Exp. 29.7% (Prev. -7.2%).

- Australian Building Permits YoY Final (Feb) Y/Y 14.0% vs. Exp. 14.0% (Prev. -15.7%).

- Japanese PPI YoY (Mar) Y/Y 2.6% vs. Exp. 2.4% (Prev. 2%).

- Japanese PPI MoM (Mar) M/M 0.8% vs. Exp. 0.9% (Prev. -0.1%).