EU Market Open: APAC stocks were mostly subdued but with downside limited; geopolitics continues to drive price action

20 Mar 2026, 06:58 by Newsquawk Desk

- The US Pentagon is considering sending more troops to the Middle East, according to Politico sources who stated the size and scope of additional deployments are still evolving.

- Saudi officials see the base case for oil to rise to USD 180/bbl if the disruptions persist until late April, according to WSJ.

- APAC stocks were mostly subdued but with downside limited as the region reacted to the recent oil swings, deluge of central bank meetings and mixed geopolitical headlines, while conditions were thinned with the absence of Japanese participants due to the Vernal Equinox holiday.

- European equity futures indicate a higher cash market open with Euro Stoxx 50 futures up 0.7%, after the cash market closed with losses of 2.1% on Thursday.

- Looking ahead, highlights include German PPI (Feb), UK PSNB (Feb), Canadian Retail Sales (Jan), PPI (Feb). Speakers include ECB's Nagel. Credit Rating Update with Scope Ratings/Morningstar DBRS on France.

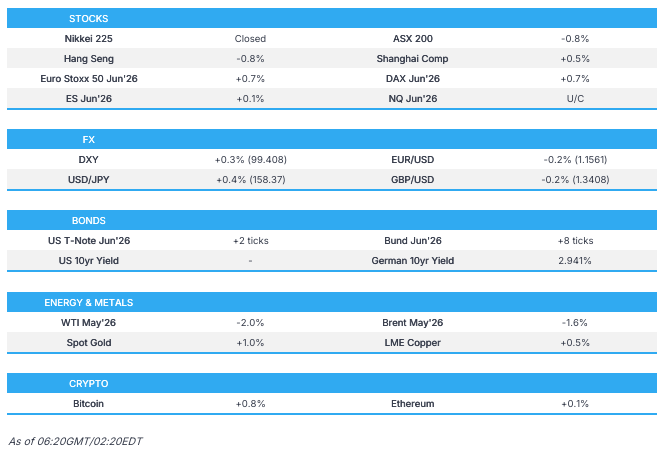

SNAPSHOT

IRAN CONFLICT

- US Pentagon is considering sending more troops to the Middle East, according to Politico sources who stated the size and scope of additional deployments are still evolving.

- Israeli PM Netanyahu said Iran has no capacity to enrich uranium or make ballistic missiles after 20 days of war, while he added the US and Israel have destroyed Iran's fleet in the Caspian and that Israel is helping the US open the Strait of Hormuz. Netanyahu also said that US President Trump asked them to hold off on the future of such attacks on the South Pars field, while he suggested it will end much sooner than people think.

- Israel’s Chief of the Joint Chiefs of Staff of the Army said that Israel has not yet reached the "halfway point" of its operations against Iran, and senior military officials have not set any immediate timetable for the end of the war.

- Israeli Broadcasting Corporation cited sources who stated the joint campaign between Israel and the US is expected to continue for several more weeks. It was separately reported that an Israeli assessment is for the continuation of the war with Iran for several additional weeks.

- IDF launched a wave of strikes on infrastructure targets across Iran, while the Israeli army later announced it was launching raids on the Iranian regime's infrastructure throughout Tehran.

- IDF identified several missiles launched by Iran towards Israel, while explosions were reported in Jerusalem, and the Israeli army said it was working to intercept missiles launched from Iran.

- Iranian media reported major attacks on Tehran and explosions heard in Kerman, southeast of the country, while an explosion was also heard in the Iranian city of Isfahan.

- Iran said it fired a fresh wave of missiles at Israel and confirmed on Thursday that it hit Israel's Haifa and Ashdod refineries with missiles, while Iran also threatened to target American and Israeli infrastructure and warned of a new escalation.

- Iran was said to allow more Indian vessels to pass through the Strait of Hormuz.

- UAE Ministry of Interior announced air defences were dealing with a missile threat.

- Kuwait's army said air defences were responding to enemy missile and drone attacks. It was later reported that the Kuwait Petroleum Corporation announced a fire affecting units of the Mina al-Ahmadi refinery following hostile attacks.

- IAEA's Grossi said he does not believe that any war will eliminate Iran's nuclear ambitions and capabilities.

- France's Foreign Minister is to visit Israel today in an effort to secure a ceasefire in Lebanon

- EU leaders called for de-escalation, civilian protection and full respect of international law by all parties, while they called for a moratorium on strikes targeting energy and water infrastructure, and strongly condemned Iran's indiscriminate strikes.

- US mediators offered Hamas a formal proposal last week to give up their weapons.

US TRADE

EQUITIES

- US stocks finished mostly in the red, but were off worst levels after remarks from Israeli PM Netanyahu, who said Iran has no capacity to enrich uranium or make ballistic missiles, sparking optimism that they are close to achieving their goals, and added that the war may be over sooner than people think. However, the rebound was capped as he added that they will continue to hunt down the leaders of the IRGC, and the campaign will take as long as necessary. His remarks spurred a further pullback in oil prices, while stocks and bonds rallied. Sectors were mostly negative, with Energy the sole outperformer as demand for refined products remains elevated, while Materials lagged as metals were hit in response to five G10 central banks (BoJ, ECB, BoE, SNB, Riksbank) following in the footsteps of the Fed on Wednesday, holding rates amid uncertainty over the economic impacts from the Middle East conflict.

- SPX -0.27% at 6,607, NDX -0.29% at 24,355, DJI -0.44% at 46,022, RUT +0.65% at 2,495.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said at a dinner with Japan's PM that the US is encouraged to see Japan buying US defence equipment.

- Japanese PM Takaichi said Japan will increase imports of oil from the US and agreed to coordinate on missile development with the US, while Japan also confirmed they will invest up to USD 73bln in reactors from GE Vernova (GEV), as well as natgas generation projects.

- US and Japan released their critical minerals cooperation plan and are to focus on initial price-floor discussions on select critical minerals, as well as discuss trade measures which can support a resilient critical minerals marketplace. Furthermore, they will identify specific critical minerals mining, processing and manufacturing projects in the US, Japan and other countries.

NOTABLE HEADLINES

- White House is expected to send Congress its ideas for regulating AI on Friday, while the AI framework will cover child safety, creators and censorship, according to Axios citing sources.

APAC TRADE

EQUITIES

- APAC stocks were mostly subdued but with downside limited as the region reacted to the recent oil swings, deluge of central bank meetings and mixed geopolitical headlines, while conditions were thinned with the absence of Japanese participants due to the Vernal Equinox holiday.

- ASX 200 was dragged lower by weakness in the materials and commodity-related sectors, but with losses cushioned by strength in telecoms and defensives, while there were few fresh drivers overnight.

- Hang Seng and Shanghai Comp were following disappointing earnings results from the likes of Alibaba and CK Hutchison, with the former posting a 67% drop in Q3 net, which also weighed on other tech names. Furthermore, the PBoC's reiteration to continue implementing a moderately accommodative monetary policy and to use RRR and MLF to ensure sufficient stability did little to inspire, while China's Loan Prime Rate were unsurprisingly kept unchanged for the 10th consecutive month.

- US equity futures were rangebound despite the brief tailwinds seen during late US trade after Israeli PM Netanyahu suggested an earlier end to the war than people think, but stated the campaign will take as long as necessary, while price action was also restricted ahead of quad witching.

- European equity futures indicate a higher cash market open with Euro Stoxx 50 futures up 0.7%, after the cash market closed with losses of 2.1% on Thursday.

FX

- DXY nursed some losses after retreating yesterday amid a slew of G10 central bank rate announcements, whereby the theme was similar to that of the Fed on Wednesday: hold for now, until gaining further clarity on economic impacts from the Middle East conflict. Furthermore, comments from Israeli PM Netanyahu, who stated that the war will end much sooner than people think, spurred risk appetite and a further deterioration in the USD.

- EUR/USD mildly pulled back overnight after briefly returning to above the 1.1600 level in the wake of the ECB meeting, where rates were kept on hold, as expected, although the announcement was somewhat skewed hawkish, given the significant upgrade to inflation projections, while ECB source reports noted officials see the need for possible rate hike talk to start in April, but added that a move would be more likely in June.

- GBP/USD trickled lower after strengthening in the aftermath of the BoE decision to keep rates unchanged, as expected, but in a more hawkish fashion with the vote unanimous at 9-0 (exp. 7-2), and the statement removed language suggesting further cuts, while it was also reported that UK ministers are to visit European capitals next week in a bid to deepen ties with the EU on financial services.

- USD/JPY partially rebounded after slumping briefly below the 158.00 handle, while the mild recovery was facilitated as the dollar regained composure, but with further momentum contained amid the absence of Japanese participants.

- Antipodeans saw mixed and rangebound trade amid the cautious risk appetite and in the absence of tier-1 data.

- PBoC set USD/CNY mid-point at 6.8898 vs exp. 6.8773 (Prev. 6.8975)

FIXED INCOME

- 10yr UST futures just about kept afloat amid declines in oil prices, but with gains limited after the recent choppy performance and curve flattening on hawkish central bank expectations in response to the Iran war, while overnight price action was also contained by the absence of cash treasuries trade due to the holiday closure in Tokyo.

- Bund futures rebounded from the prior day's trough, albeit with the upside contained following hawkish ECB reports.

COMMODITIES

- Crude futures continued to retreat from yesterday's peak with fluctuation in prices at the whim of supply and geopolitical-related headlines including comments from US Treasury Secretary Bessent that the US could do another SPR release to keep prices down and may un-sanction Iranian oil, while the White House will reportedly not implement a crude export ban, and Chevron is restarting the jet fuel unit at its El Segundo refinery. Furthermore, Israeli officials confirmed the attack on Iran's South Pars gas field will likely not be repeated, and Israeli PM Netanyahu said the war will end sooner than people think.

- Saudi officials see the base case for oil to rise to USD 180/bbl if the disruptions persist until late April, according to WSJ

- US Energy Secretary Wright said the Trump administration has no plan to implement restrictions on oil and gas exports, while US lawmakers are said to be in talks about energy permitting reforms.

- EU member states are to request that the European Commission design national temporary and targeted measures to mitigate impacts related to energy costs, according to a draft document.

- Spot gold nursed some losses after its recent slide to briefly test the USD 4,500/oz level, where support held, although the precious metal was still seen on course for its worst weekly loss in six years after the recent deluge of central bank updates, which were hawkish-leaning, given the inflationary pressures from the war-driven oil surge.

- Copper futures rebounded from yesterday's intraday dip, but with further upside capped by the lacklustre risk environment.

CRYPTO

- Bitcoin steadily gained and approached the USD 71,000 level before mildly pulling back from intraday highs.

NOTABLE ASIA-PAC HEADLINES

- Chinese Loan Prime Rate 1Y (Mar) 3.00% vs. Exp. 3.00% (Prev. 3.00%)

- Chinese Loan Prime Rate 5Y (Mar) 3.50% vs. Exp. 3.50% (Prev. 3.50%)

- China's government is reportedly being urged to reform the consumption tax in order to boost local income, according to China's Securities Journal.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian President Zelensky said Ukrainian negotiators are to hold talks in the US on Saturday.

- German Chancellor Merz said EU leaders have asked the European Commission to examine other possible ways of paying out loans to Ukraine.

OTHER NEWS

- US President Trump could buy the Chagos Islands if the UK’s handover deal with Mauritius collapses, according to sources cited by The Sun.

EU/UK

NOTABLE HEADLINES

- UK may delay shipbuilding plans amid GBP 10bln defence budget cut, according to The Times.

- European Council appointed ECB's Vujcic as the central bank's Vice President to replace de Guindos as of June 1st.

- ECB's Stournaras said the Iran conflict could have a large macroeconomic impact and the Middle-East conflict is an adverse supply shock, while he added the EU should issue debt jointly to finance defence, green transition, and strategic investment.