US Market Open: US equities set to open with modest gains as markets wait for September US PCE

05 Dec 2025, 11:48 by Newsquawk Desk

- European bourses trade modestly firmer, with little macro news to steer price action. Sentiment follows on from a mixed and quiet APAC session.

- US equity futures are mixed/mostly firmer with a skew towards tech-positive as ES and NQ eke mild gains vs the YM and RTY.

- DXY has unwound most of its earlier losses. Initially hit by a firmer JPY on the back of more hawkish BoJ sources, coupled with verbal intervention; USTs remain flat in a thin 112-22+ to 112-27+ band.

- Baidu (9888 HK/ BIDU) reportedly weighs a Hong Kong IPO for its AI chip unit Kunlunxin, to rival NVIDIA (NVDA); Dell (DELL) reportedly plans price hike of 15-20% from mid December.

- A Russian Kremlin aide said Russia and the US are moving forward in talks relating to Ukraine. Ready for further work with the current US negotiating team.

- Looking ahead, highlights include Canadian Jobs Report (Nov), US PCE (Sep), US University of Michigan Prelim (Dec), Comments from ECB's Lane.

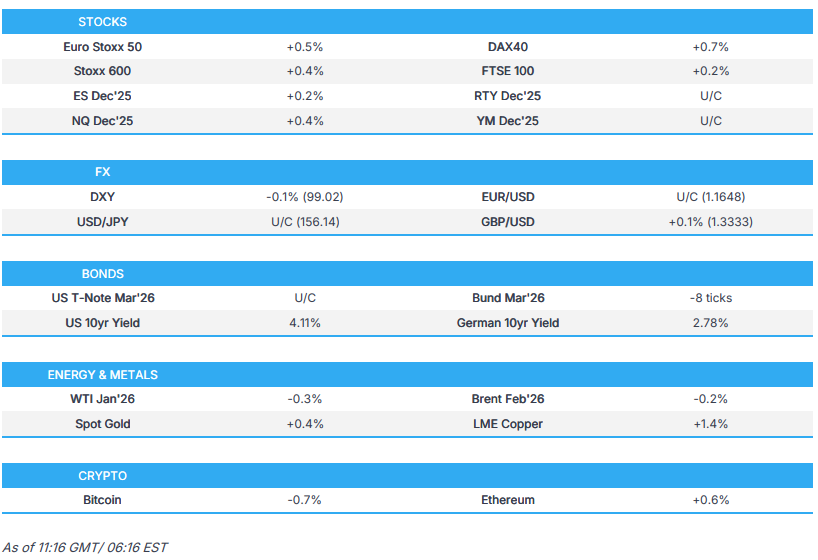

SNAPSHOT

TARIFFS/TRADE

- US Trade Representative Greer said trade with China needs to be balanced and probably needs to be smaller, while he added they want to have stability in the relationship with China, and that the US trade deficit in goods with China is down about 25%, which is the right direction.

- USTR Greer also noted there are problems with the US-Mexico-Canada Trade Agreement and that they already have adjustments to some of these challenges, as well as stated that the US wants to make sure that Canada and Mexico aren't used as an export hub for China, Vietnam or Indonesia, among others.

- China's Foreign Ministry Spokesperson said that China has repeatedly stated its position on the issue of US chip exports to China, via Global Times.

- Chinese drone maker DJI urged the Trump administration to complete audits or extend the deadline for the security review, according to a letter to Congress.

- China and France issued a joint statement on agricultural cooperation and signed an MOU on registration of infant milk powder formulas, according to Xinhua.

- Japanese Trade Minister Akazawa said they are monitoring US tariff lawsuit developments and he confirmed that Japanese companies have filed lawsuits in the US seeking refunds of additional tariffs.

- Russian President Putin said Russia is ready to provide uninterrupted fuel supplies to India. Russia and India express interest in deepening cooperation in the exploration, processing and refining technologies for critical minerals and rare earths.

NOTABLE US HEADLINES

- Morgan Stanley forecasts a 25bps Fed cut in December (prev. forecast unchanged). Cuts in January and April 2026, a terminal of 3.00-3.25%.

- Bank of America (BAC) CEO said US consumer spending was good during November, via Bloomberg TV.

- Federal Reserve Board announced a new pricing for payment services provided to banks and credit unions, effective 1st January 2026, while Fed's Bowman emphasised the importance of checks as a payment method and said the Fed cannot endorse the RFI regarding the future of check services.

- US Supreme Court revived the redrawn pro-Republican Texas voting map intended to help Republicans keep control of Congress.

- US Homeland Security Secretary Noem said the Trump administration is expanding the countries on the travel ban to over 30, according to Fox News.

NOTABLE EQUITY NEWS

- Dell (DELL) reportedly plans a price hike of 15-20% from mid-December and Lenovo (992 HK) from January 2026, according to TrendForce, citing sources.

- Cloudflare (NET) announced service issues have been resolved, according to the status page. Following issues that lasted for around 30 minutes.

- Baidu (9888 HK/ BIDU) reportedly weighs a Hong Kong IPO for its AI chip unit Kunlunxin, to rival NVIDIA (NVDA), according to Bloomberg, citing sources; unit could be valued in excess of USD 3bln

- Apple (AAPL), Google (GOOGL) and Samsung (005930 KS) have asked the Indian Government not to accept telecom proposal over privacy concerns and regulatory overreach, according to Reuters, citing sources.

EUROPEAN TRADE

EQUITIES

- European bourses trade modestly firmer, with little macro news to steer price action. Sentiment follows on from a mixed and quiet APAC session.

- European sectors mostly reside in the green, led by Financial Services, Basic Resources, Construction and Chemicals. Higher metal prices—particularly copper—help underpin sentiment in Basic Resources, while broader macro flow remains light.

- US equity futures are mixed/mostly firmer with a skew towards tech-positive as ES and NQ eke mild gains vs the YM and RTY. Premarket headlines note that Dell is reportedly planning a mid-December price hike between 15-20%. Focus now turns to the September US PCE.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY has unwound most of its earlier losses. Initially hit by a firmer JPY on the back of more hawkish BoJ sources, coupled with verbal intervention (see below for details). The JPY reaction took DXY down to a 98.805 intraday trough (vs 99.075 APAC high), although since newsflow quietened and despite a stable risk environment, the JPY waned and DXY now attempts to reclaim 99.00 to the upside at the time of writing. The index, however, remains within yesterday's 98.765-99.08 ahead of the September US PCE, which was delayed by the US government shutdown.

- JPY has surrendered most of its earlier gains after an initial surge triggered by Bloomberg sources suggesting the BoJ is likely to hike this month while keeping the door open to further tightening. The reports briefly pushed USD/JPY below 154.50. This was followed by verbal intervention from Chief Cabinet Secretary Kihara, who reiterated that authorities would take appropriate steps against excessive or disorderly FX moves if needed. USD/JPY subsequently touched a 154.34 low before rebounding and stalling just shy of 155.00, despite limited follow-through newsflow and a stable risk backdrop.

- AUD is the top gainer, lifted by a surge in copper prices and earlier USD softness, though both AUD and copper later eased off highs as the dollar attempted a recovery. The AUD/NZD cross extended its rebound, pushing back above 1.1450 and trading toward the upper end of a 1.1461–1.1484 range.

- Other G10s vary and continue to take their cue from broader USD moves, though EUR saw a couple of brief upticks after slight upward revisions to Eurozone Q3 GDP and Employment. EUR/USD now trades mid-range within 1.1640–1.1672.

- PBoC set USD/CNY mid-point at 7.0749 vs exp. 7.0745 (Prev. 7.0733)

FIXED INCOME

- USTs remain flat in a thin 112-22+ to 112-27+ band. Traders look ahead to US PCE at 15:00 GMT / 10:00 ET, a release that will feed into the debate around a potential December Fed cut. Odds of such a move have climbed above 85% in recent sessions, up from the low-60% range a month ago, aided by comments from Fed’s Williams, who said policymakers have room for another adjustment in the “near term.”

- JGBs were hit overnight on further hawkish BoJ source reports, with market-implied odds of a December hike nearing 80%. The 10yr Japanese future fell over 20 ticks to a 133.91 trough before stabilising. Since then, bonds have held in tighter ranges as attention turns to US PCE.

- Bunds were marginally softer in a 128.29–128.52 range as markets awaited the 11:30 GMT Bundestag pension vote, which is now widely expected to pass after Die Linke signalled it will abstain—lowering the effective majority threshold and reducing the relevance of dissent within the CDU/CSU’s Young Group. The vote remains a key barometer of Chancellor Merz’s coalition stability.

COMMODITIES

- WTI and Brent continue to trade in tight ranges with European trade underway, and following an overnight session devoid of crude-specific catalysts. Early-door comments from a Kremlin aide noted that Russia and the US are progressing in Ukraine-related talks and that Moscow is ready for further engagement, though this echoed recent rhetoric and left crude benchmarks largely unreactive pending fresh developments.

- Spot Gold found support near USD 4,200/oz in early APAC trade and steadily climbed to a USD 4,231/oz peak as Europe opened. The overnight bid was helped by weakness in the Dollar, with JPY strength driven by reports of a potential December BoJ rate hike. Since the European open, the Dollar has begun to recover, but XAU continues to hold near session highs.

- 3M LME Copper extended its rally to fresh record highs after Thursday’s consolidation in a tight USD ~180/t band. The contract opened just below USD 11.45k/t before buyers immediately stepped in, driving prices to a new all-time high at USD 11.7k/t as Europe opened.

- Discounts for Russian ESPO blend crude oil delivered to China have widened to USD 5-6/bbl vs ICE Brent due to falling demand, according to Reuters

NOTABLE DATA RECAP

- EU Employment Final YY (Q3) 0.6% vs. Exp. 0.5% (Prev. 0.5%)

- EU GDP Revised YY (Q3) 1.4% vs. Exp. 1.4% (Prev. 1.4%)

- EU GDP Revised QQ (Q3) 0.3% vs. Exp. 0.2% (Prev. 0.2%)

- EU Employment Final QQ (Q3) 0.2% vs. Exp. 0.1% (Prev. 0.1%)

- UK BBA Mortgage Rate (Nov) 6.81% (Prev. 6.78%, Rev. 6.81%)

- UK Halifax House Prices MM (Nov) 0.0% (Prev. 0.6%, Rev. 0.5%)

- UK Halifax House Prices YY (Nov) 0.7% (Prev. 1.90%)

- German Industrial Orders MM (Oct) 1.5% vs. Exp. 0.4% (Prev. 1.1%)

- Spanish Ind Output Cal Adj YY (Oct) 1.2% (Prev. 1.7%, Rev. 1.5%)

- French Trade Balance, EUR, SA (Oct) -3.92B (Prev. -6.58B, Rev. -6.35B)

- French Imports, EUR (Oct) 55.648B (Prev. 58.495B, Rev. 58.314B)

- French Exports, EUR (Oct) 51.73B (Prev. 51.919B, Rev. 51.967B)

- French Current Account (Oct) 1.1B (Prev. -1.6B)

- French Industrial Output MM (Oct) 0.2% vs. Exp. -0.1% (Prev. 0.8%, Rev. 0.7%)

- Italian Retail Sales NSA YY (Oct) 1.3% (Prev. 0.5%)

- Italian Retail Sales SA MM (Oct) 0.5% (Prev. -0.5%)

NOTABLE EUROPEAN HEADLINES

- Regulators at the BoE announce plans to support the growth of the mutuals sector. Measures include: A PRA and FCA review of mutual credit union regulations, considering more risk-based requirements for larger, complex firms and proportionality for smaller credit unions.

GEOPOLITICS

MIDDLE EAST

- Hamas Leader to Al-Arabiya: "The Movement Does Not Want to Continue to Rule Gaza ... We Agreed to Form a Technocratic Committee to Govern Gaza".

- US President Trump plans to announce before Christmas the transition to phase 2 of the agreement to end the war in Gaza and the establishment of the new governing body that will manage the strip, according to Axios's Ravid.

RUSSIA/UKRAINE

- Russia's Kremlin said Moscow is waiting for the US reaction after Putin-Witkoff meeting, while it added that there is no plan for a Putin-Trump call for now.

- Russian Kremlin aide said Russia and the US are moving forward in talks relating to Ukraine. Ready for further work with the current US negotiating team.

- The US has urged the EU to oppose the plan to use frozen Russian central bank assets to back a massive loan to Ukraine, via Bloomberg Sources.

- UK ministers are prepared to unlock GBP 8bln of frozen Russian assets to aid Ukraine, according to The Times.

OTHER NEWS

- US military said it conducted a lethal kinetic strike on a vessel in international waters in the eastern Pacific on Thursday.

CRYPTO

- Crypto markets are mixed/subdued, with Bitcoin still trading below USD 92,000 while Ethereum holds around USD 3,150.

APAC TRADE

EQUITIES

- APAC stocks were mixed with the regional bourses mostly rangebound, amid light fresh catalysts ahead of US PCE data.

- ASX 200 edged higher but with gains capped as strength in the mining and materials sectors was partially offset by weakness in consumer discretionary, energy and telecoms, while price action was also contained by the absence of any pertinent data.

- Nikkei 225 underperformed amid the increased BoJ December rate hike bets and after dismal Household Spending data, which showed a surprise contraction.

- Hang Seng and Shanghai Comp saw two-way price action with early headwinds following another consecutive liquidity drain by the PBoC and reports that US senators seek to block NVIDIA (NVDA) sales of advanced chips to China for 30 months, which would target NVIDIA's H200 and Blackwell chips.

NOTABLE ASIA-PAC HEADLINES

- BoJ is said to likely hike this month and leave the door open to more, while the central bank is to check the data and market moves up to the final decision, according to Bloomberg.

- Japan's Chief Cabinet Secretary Kihara said they will take appropriate steps on excessive and disorderly moves in the FX market if necessary. Expects the BoJ to conduct monetary policy in an appropriate manner.

- Japan's Economy Minister Kiuchi said the inflationary impact of the stimulus package will likely be limited. The government will keep an eye on market moves with a high sense of urgency. Important for stocks, FX and bond markets to move in line with fundamentals. Specific monetary policy means is up to the BoJ, and the Government will not comment. Hopes the BoJ guides appropriate monetary policy to stably achieve the 2% inflation target.

- Hong Kong's Court endorsed a proposal allowing Country Garden Holdings (2007 HK) to extend repayment of USD 17.7bln in offshore debt.

- China's Commerce Minister said China will ramp up efforts to expand imports, via Xinhua. The Commerce Minister will also expand service consumption, increase implementation of inclusive policies that directly reach consumers, expand auto consumption and promote renewal consumption of home appliances and eliminate restrictive measures.

- RBI cut the Repurchase Rate by 25bps to 5.25%, as expected, with the decision unanimous and it maintained a neutral stance although MPC member Ram Singh wanted the stance to be changed to accommodative from neutral, while the Marginal Lending Facility Rate was lowered by 25bps to 5.50% and the Standing Deposit Facility Rate was reduced by 25bps to 5.00%.

DATA RECAP

- Japanese All Household Spending MM (Oct) -3.5% vs. Exp. 0.7% (Prev. -0.7%)

- Japanese All Household Spending YY (Oct) -3.0% vs. Exp. 1.0% (Prev. 1.8%)

- Hungarian Industrial Output YY (Oct) -2.7% vs. Exp. -3.8% (Prev. 1.3%)