Europe Market Open: Biden drops out of the presidential race; APAC stocks mostly began the week on the back foot

22 Jul 2024, 06:36 by Newsquawk Desk

- US President Biden has dropped out of the Presidential race and endorsed VP Harris

- PBoC surprised markets by cutting its 7-day reverse repo rate by 10bps

- APAC stocks mostly began the week on the back foot after last Friday's selling pressure on Wall St

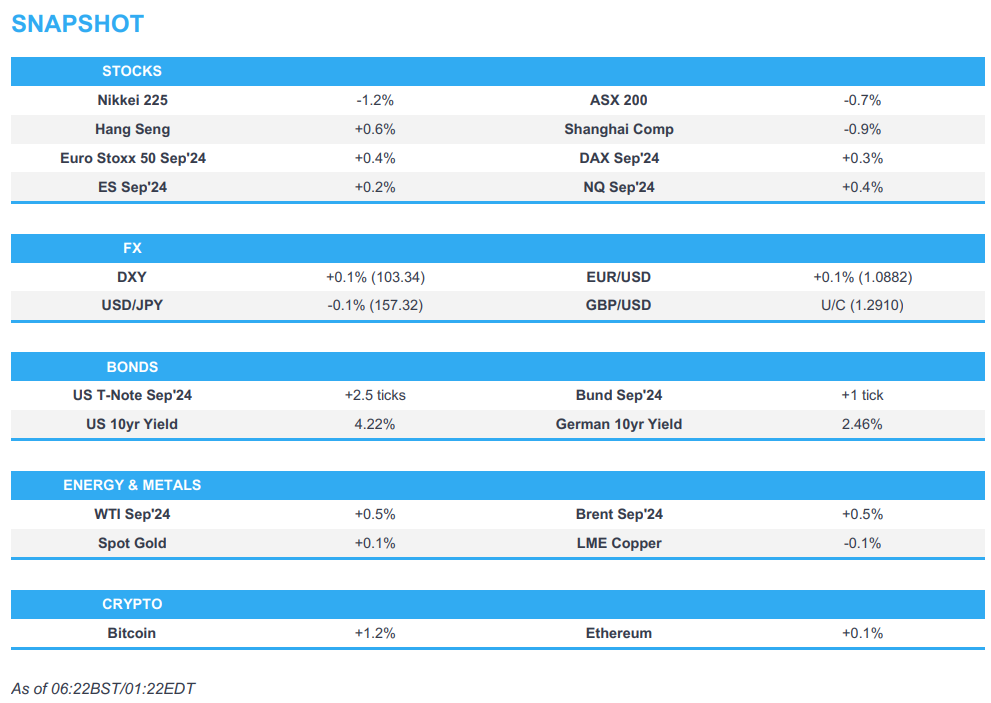

- European equity futures indicate a higher open with Euro Stoxx 50 futures up 0.5% after the cash market finished lower by 0.9% on Friday

- DXY is steady and in a tight range, EUR/USD sits on a 1.08 handle, antipodeans lag

- Looking ahead, highlights include German Retail Sales

US TRADE

EQUITIES

- US stocks continued their slide on Friday as a global IT outage sparked by a CrowdStrike (CRWD) update weighed on risk sentiment and President Biden's re-election chances continued to dwindle, while crude prices tumbled throughout the session and the buck was underpinned amid higher yields and the risk-off trade.

- SPX -0.71% at 5,505, NDX -0.93% at 19,523, DJIA -0.93% at 40,288, RUT -0.63% at 2,184

- Click here for a detailed summary.

NOTABLE HEADLINES

- US President Biden announced he is stepping aside as a candidate and will focus on fulfilling his duties for the remainder of his term, while he endorsed Vice President Harris and will speak to the nation later this week.

- US Vice President Harris said she is honoured to have the President’s endorsement and she intends to earn and win the nomination, while she added that she will do everything in her power to unite the Democratic Party and unite the nation to defeat Donald Trump.

- Super PAC Priorities USA and liberal super PAC Unite the Country said they will support Kamala Harris as the 2024 Democratic presidential nominee, while Bill and Hillary Clinton announced their endorsement of Harris. It was separately reported by CBS News that California Governor Newsom and Michigan Governor Whitmer do not plan to challenge Harris and Newsom later endorsed Harris for the Democratic Presidential nomination.

- Democratic National Committee Chair Harrison said the American people will hear from the Democratic Party on the next steps and the path forward for the nomination process.

- Independent Senator Manchin is weighing to re-register as a Democrat as part of a potential bid to replace Biden as candidate, according to a source familiar cited by Reuters

- Republican presidential candidate Donald Trump said he thinks that Kamala Harris will be easier to defeat than President Biden in the November election, according to a CNN reporter via X.

APAC TRADE

EQUITIES

- APAC stocks mostly began the week on the back foot after last Friday's selling pressure on Wall St and despite China’s surprise cuts, while markets also reflected on President Biden's decision to bow out of the election race.

- ASX 200 was led lower by the commodity-related sectors with energy the worst hit after oil prices tumbled on Friday, while miners also suffered including South32 with its shares down by a double-digit percentage following its output update where it also flagged an impairment charge of USD 554mln for its Worsley Alumina operations.

- Nikkei 225 extended on its recent declines after gapping beneath the key 40,000 level.

- Hang Seng and Shanghai Comp. were mixed in which the former bucked the trend owing to the resilience in local tech-related stocks, while the mainland was pressured after President Xi noted China’s development entered a period of coexistence of strategic opportunities, risks and challenges, as well as increasing uncertainties and unpredictable factors. Furthermore, the PBoC’s surprise announcement to cut its 7-day reverse repo rate by 10bps, which Chinese banks followed through with similar cuts to the benchmark LPRs, failed to spur risk appetite as some viewed the cut to short-term funding rates as underwhelming and not the big measures needed to revive the economy and China’s slowing property industry.

- US equity futures were marginally higher in some mild respite from the selling pressure during the tail end of last week.

- European equity futures indicate a higher open with Euro Stoxx 50 futures up 0.5% after the cash market finished lower by 0.9% on Friday.

FX

- DXY saw two-way price action but was contained within tight parameters as the initial mild weakness following the announcement of President Biden bowing out of the election race, was partially reversed, while there was a lack of conviction ahead of key data releases from the US later this week and with the Fed on a blackout period.

- EUR/USD eked marginal gains amid early dollar pressure and after comments over the weekend from ECB’s Makhlouf who suggested there is no need to rush on deciding on a rate cut. However, the single currency then mildly pulled back after failing to sustain a brief foray into 1.0900 territory.

- GBP/USD traded rangebound and remained above near-term support at the 1.2900 level, while reports over the weekend noted that UK Treasury ministers are softening up public opinion for a tough autumn Budget and potential tax increases.

- USD/JPY mirrored the indecisive mood in the dollar as participants reflected on the ongoing political uncertainty in the US and amid a lack of Japanese data releases.

- Antipodeans reversed initial advances amid headwinds from the subdued risk tone and recent commodity weakness.

- PBoC set USD/CNY mid-point at 7.1335 vs exp. 7.2624 (prev. 7.1315)

FIXED INCOME

- 10-year UST futures lacked direction as participants digested President Biden’s decision to drop out of the election race, while participants look ahead to this week’s supply and data releases including advanced Q2 GDP and the latest PCE prices.

- Bund futures traded little changed and remained just above the 132.00 level ahead of German Retail Sales data.

- 10-year JGB futures attempted to claw back Friday’s after-hour losses but with price action contained amid a light calendar and after the minutes from the BoJ’s meeting with bond market participants earlier this month provided little fresh insight into actual BoJ thinking, while the latest enhanced liquidity auction for 2yr-20yr JGBs resulted in a lower bid-to-cover

COMMODITIES

- Crude futures nursed some of Friday's hefty losses but with the rebound limited amid a lack of energy-specific drivers with the WTI September contract languishing firmly beneath the USD 80/bbl level.

- Dubai set official crude differential to DME Oman for October at USD 0.10/bbl premium.

- Spot gold marginally rebounded off last week’s trough and just about reclaimed the USD 2,400/oz status.

- Copper futures lacked direction with price stuck around a 3-month low amid the mostly subdued risk appetite in Asia despite the PBoC’s surprise rate cuts.

CRYPTO

- Bitcoin mildly weakened and dipped beneath the USD 68,000 level to pare some of its weekend advances.

NOTABLE ASIA-PAC HEADLINES

- PBoC 1-Year Loan Prime Rate (Jul) 3.35% vs Exp. 3.45% (Prev. 3.45%)

- PBoC 5-Year Loan Prime Rate (Jul) 3.85% vs Exp. 3.95% (Prev. 3.95%)

- China will change the release time of the monthly LPR fixing to 09:00 local time (02:00BST/21:00EDT) from 09:15 local time (02:15BST/21:15EDT) on the 20th of each month.

- PBoC announced a cut to the 7-day reverse repo rate to 1.70% from 1.80% and will strengthen counter-cyclical adjustment to better support the real economy, while it is to lower collateral requirements for the Medium-term Lending Facility Loans from July with the move meant to increase the size of tradable bonds in the market and to alleviate pressure on supply and demand of bonds in the market.

- Chinese President Xi said China’s development has entered a period of coexistence of strategic opportunities, risks and challenges, increasing uncertainties and unpredictable factors, while he added that various black swan and grey rhinoceros events may occur at any time, according to state media.

- China’s reform plan will push the collection stage of the consumption tax back and delegate it to local governments steadily, while it will study merging urban maintenance, construction tax, education surcharge and local education surcharge into a local surcharge and authorise local governments to determine specific applicable tax rates within a certain range. China will improve the coordination of investment and financing in the capital market, prevent risks, strengthen supervision and promote the market’s healthy and stable development. Furthermore, China will create a market-oriented, law-based and internationalised first-class business environment, while it will protect the rights and interests of foreign investment in accordance with the law.

GEOPOLITICAL

MIDDLE EAST

- Israeli military called on Gazans to clear out of eastern parts of the Khan Younis ahead of a 'forceful' operation which comes after 'significant terrorist activity and rocket fire'.

- Israel conducted a strike on Yemen’s Hodeidah on Saturday which killed six people and injured 80, while it was separately reported that Yemen’s Houthis said they fired missiles at Israel’s Eilat.

- Israeli PM Netanyahu will meet with US President Biden on Tuesday, while Netanyahu said the port that Israel conducted a strike on was an entry port for weapons from Iran and the port attack reminds enemies that there is no place that Israel cannot reach. Israeli PM Netanyahu also said Israel will send a delegation to hostage deal talks on Thursday.

OTHER

- Ukrainian President Zelensky called for long-range weapons after drone attacks on Kyiv. In relevant news, Russia's Defence Ministry announced their forces captured two settlements in Ukraine.

- Philippine Foreign Ministry said China and the Philippines reached an understanding on a provisional arrangement for resupply missions in the disputed South China Sea shoal.

EU/UK

NOTABLE HEADLINES

- UK Chancellor Reeves said she will consider inflation-busting pay rises for almost 2mln public sector workers this month to avert crippling strikes, according to Reuters.

- UK Treasury ministers are reportedly softening up public opinion for a tough autumn Budget and potential tax increases, while Chancellor Reeves said she wanted to “level” with the public about the fiscal “mess”, according to FT.

- ECB’s Makhlouf said there is no need to rush to make decisions and that rapid interest-rate action from the central bank is not required, according to an interview with the Irish Examiner.