US Market Open: US equity futures in the green, USD softer & Crude bid amid heightened geopol tensions; Fed speak due

28 May 2024, 11:05 by Newsquawk Desk

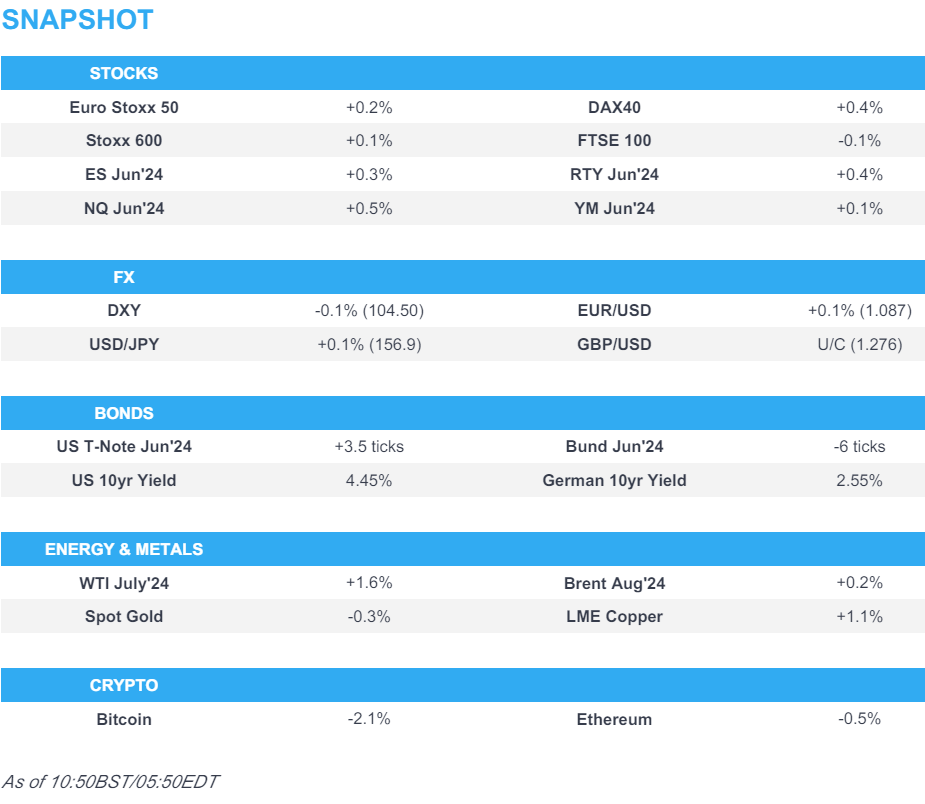

- European bourses are mixed continuing the price action seen in APAC; US equity futures are in the green

- Dollar is flat/softer, Kiwi the G10 outperformer after strong price action overnight and in continuation of the RBNZ last week

- USTs/Bunds are mixed and relatively contained, whilst Gilts outperform playing catch-up to Bund strength in the prior session

- Crude benefits from heightened geopol tensions, XAU dips and base metals are firmer across the board following the announcement of China’s USD 47.5bln chip fund

- Looking ahead, Canadian Producer Prices, Comments from ECB's Knot, Centeno, Fed’s Kashkari, Cook & Daly, and Supply from the US

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx 600 (U/C) are mixed and trade modestly on either side of the unchanged mark, continuing the tentative price action seen in APAC trade overnight.

- European sectors are mixed; Real Estate takes the top spot, benefitting from the relatively lower yield environment, whilst Travel & Leisure is weighed on by broader strength in crude prices.

- US Equity Futures (ES +0.3%, NQ +0.5%, RTY +0.5%) are indicative of a firmer open, after US markets were shut on Monday on account of Memorial Day. Apple (+1.6% pre-market) gains following reports that China iPhone shipments rose 52% in April.

- Click here for the sessions European pre-market equity newsflow and here for additional news.

- Click here for more details.

FX

- DXY is relatively flat/contained trade thus far with the index currently within a 104.41-56 band and as such is in close proximity to its 200 DMA at 104.37.

- Modest strength in the EUR which was relatively unreactive to upticks in German Wholesale Prices and to the the ECB SCE which saw the inflation view revised lower; EUR/USD trades within a 1.0855-79 range, and off best levels.

- GBP is flat vs the USD and modestly softer against the EUR. Cable sits in a 1.2764-83 parameter after briefly topping yesterday's 1.2777 high.

- JPY is slightly softer vs the USD and losing against the EUR, AUD, and GBP despite the hotter-than-expected Japanese Services PPI overnight and the currency jawboning by Finance Minister Suzuki overnight. USD/JPY currently just shy of 157.00.

- Upward bias across antipodeans following the overnight rebound in commodities. The Kiwi narrowly outperforms in a continuation of last week's hawkish hold by the RBNZ.

- PBoC set USD/CNY mid-point at 7.1101 vs exp. 7.2402 (prev. 7.1091).

- Click here for more details.

- Click here for Opex details.

FIXED INCOME

- USTs are modestly firmer but with action relatively sparse and overall rangebound into a particularly busy week highlighted by PCE on Friday; docket for today is sparse, but focus will be on US 2yr & 5yr supply. Currently trading within a tight 108-28+ to 108-22 range.

- Bunds are contained after lifting to a 130.52 peak on Monday, a high driven by remarks from ECB's Lane who in a Dublin speech/FT interview outlined that the ECB is "barring major surprises" ready to begin easing. The ECB SCE saw saw lower inflation views at both the one- & three-year ahead timeframes, an update which was enough to lift Bunds to a 130.43 peak for today vs current 130.32.

- Gilts are outperforming as the UK catches up to Monday's EGB move, with UK-specifics light except for reports via the FT which note that Sunak is to announce a GBP 2.4bln tax cut for pensioners, a development which seemingly hasn't had any bearing on Gilts given opposition Labour is well ahead in the polls. Gilts are holding above 97.00, just off the 97.14 session high.

- Italy sells EUR 4.5bln vs exp. EUR 3.75-4.5bln 3.20% 2026 & 0.00% 2024 BTP Short Term and EUR 1.5bln vs exp. 1.0-1.5bln 0.10% 2033 I/L.

- Germany sells EUR 0.846bln vs exp. EUR 1bln 2.30% 2033 Green Bund and EUR 0.986bln vs exp. EUR 1bln 2.10% 2029 Green:

- Click here for more details.

COMMODITIES

- WTI and Brent are both holding on to the prior day's gains but with a discrepancy in terms of intraday price changes amid the lack of WTI settlement yesterday as US markets were closed on account of Memorial Day. The complex was lifted amid heightened geopolitical escalations, following recent Israeli strikes on Rafah. Brent August in a USD 82.76-83.11/bbl intraday parameter.

- Precious metals are weaker across the board despite the softer Dollar, with no obvious reason for the weakness aside from the pullback in precious metals. XAU sits within a USD 2,340.79-2,356.44/oz parameter.

- Firmer across the board with base metals rebounding; desks are citing positive sentiment underpinned by the announcement of China's USD 47.5bln chip fund.

- UBS expects OPEC+ to extend current production cuts for at least another three months; says oil remains a valid geopolitical hedge - sees Brent USD 87/bbl by year-end

- Click here for more details.

CRYPTO

- Bitcoin is softer and holds just above USD 68k after surging past USD 70k in the prior session; Ethereum fares better and is just shy of USD 3.9k.

NOTABLE DATA RECAP

- UK BRC Shop Price Index YY (May) 0.6% vs Exp. 1.0% (Prev. 0.8%)

- German Wholesale Price Index YY (Apr) -1.8% (Prev. -3.0%); Wholesale Price Index MM (Apr) 0.4% (Prev. 0.2%)

NOTABLE EUROPEAN HEADLINES

- ECB Consumer Expectations Survey (Apr): 12-month inflation 2.9% (prev. 3.0%); 3-year ahead 2.4% (prev. 2.5%); growth outlook less negative and labour market seen stable

- UK PM Sunak is to announce a GBP 2.4bln tax cut for pensioners in a bid to shore up the key Conservative 'grey vote' and stabilise the party's chaotic start to the general election campaign, according to FT.

- Statistics Norway Oil Investment Survey: Total investments in oil and gas activity in 2025, including pipeline transportation, are estimated at NOK 216 billion, +5.2% than estimated in the previous quarter.

- UK Shadow Chancellor Reeves says Labour will not be matching the "Triple Lock Plus"

NOTABLE US HEADLINES

- China's smartphone market saw a 2% growth in sales Q1. Sales of foldable phones +48% Y/Y. Huawei rose to the top spot for the first time in quarterly global shipments, surpassing Samsung, according to Counterpoint Research. China iPhone shipments jump 52% in April.

- UBS Global Research raises 2024 year-end S&P500 target to 5600 (prev. target 5400, current 5304)

GEOPOLITICS

MIDDLE EAST - EUROPEAN MORNING

- Israeli tanks have reached Rafah city centre, according to Reuters witnesses

- "Israeli media: Leaders of Israeli opposition parties will discuss tomorrow the formation of an alternative government and the ouster of Netanyahu", according to Sky News Arabia.

- Ambrey says it is aware of incident 54NM southwest of Yemen's Hodeidah, according to advisory.

MIDDLE EAST

- Israeli PM Netanyahu said something went tragically wrong regarding the Israeli air strike on Rafah and it will be investigated, while Israel’s government said initial reports are that Rafah civilians died from a fire that broke out after an Israeli strike on Hamas chiefs.

- Israeli PM Netanyahu reportedly intends to dissolve the War Council so that he does not have to include Ben-Gvir and Smotrich in it, according to the Israel Broadcasting Corporation.

- Israel is waiting to hear Hamas’s stance before deciding on re-joining hostage talks, according to Times of Israel.

- Palestinian media reported intensive Israeli shelling in the vicinity of the Emirati hospital west of Rafah in the southern Gaza Strip, according to Al Arabiya.

- Pro-Iranian militias in Iraq claimed responsibility for launching three drones at military targets in Eilat, while Israel said three drones launched from Iraq were intercepted.

- White House noted devastating images following the Israeli strike in Rafah on Sunday, while it is actively engaging the IDF and partners on the ground to assess what happened. Furthermore, the White House said Israel must take every precaution possible to protect civilians.

- French President Macron said he is outraged by the Israeli strikes that have killed many displaced persons in Rafah and called for these operations to stop.

- EU’s Borrell said he is horrified by news out of Rafah regarding Israeli airstrikes killing dozens of displaced persons including small children and condemned this in the strongest terms, while he called for attacks to stop immediately. EU Borrell also stated that he has the green light from EU ministers to reactivate the Rafah border mission.

- UN Secretary-General Guterres said they condemned Israel’s practices that led to the killing of dozens of innocent people seeking shelter from the conflict and called for the terror to stop, according to Reuters.

- An Egyptian soldier was killed in a clash with Israeli troops at a crossing on Monday, according to Bloomberg.

- Yemen’s Houthis said they launched attacks on three ships in the Indian Ocean and Red Sea, while Houthis also stated that they targeted two US destroyers in the Red Sea, according to Reuters.

- IAEA report stated that Director General Grossi deeply regrets that Iran has not reversed its decision to bar several experienced inspectors, while it noted that outstanding safeguard issues including uranium traces at undeclared sites remain unresolved. It also stated that according to the IAEA’s definition, Iran’s stock of uranium enriched up to 20% is theoretically enough to produce a nuclear bomb if enriched further, according to Reuters.

OTHER

- Ukrainian President Zelensky will visit Belgium on Tuesday to sign the latest in a string of security accords with Western allies, according to the Belgian PM's office cited by Reuters.

- Ukrainian commander said French military instructors are to visit Ukrainian training centres, according to Reuters.

- Russia’s Foreign Ministry said Russia will respond to the restriction on Russian diplomats’ movement in Poland, according to TASS.

- China’s Foreign Ministry said US lawmakers paid a visit to Taiwan despite China’s strong opposition and it urged them to stop playing the Taiwan card and stop using excuses to interfere in China’s internal affairs, while it also lodged stern representations against the visit, according to Reuters.

- China and the US held talks on maritime issues and exchanged views on May 24th, while they will continue negotiations to avoid a misunderstanding and agreed to manage maritime risks, according to China's Foreign Ministry. Furthermore, China and the US agreed to maintain dialogue and China urged the US to refrain from intervening in maritime disputes between China and its neighbours, while it added the US should refrain from ganging up to 'use the sea to control China' and should immediately stop supporting and condoning 'Taiwan independence' forces.

- China Maritime Safety Authority said China is to conduct military exercises in the Yellow Sea between May 28th and June 3rd and will conduct sea rocket launches in the Yellow Sea on May 28th-31st, according to Reuters.

- North Korea launched a rocket carrying a spy satellite which exploded in the first stage of the launch. South Korea and Japan condemned North Korea’s launch, while the US said North Korea’s launch is a brazen violation of UN Security Council resolutions and raises tensions. Furthermore, the launch was said to have involved technologies directly involved in North Korea’s ICBM program and the US is assessing the situation but noted that the launch did not pose an immediate threat, according to Reuters.

CENTRAL BANKS

- Fed's Kashkari (non-voter) says inflation has moved sideways recently; need to wait and see and get more confidence on prices; should not rule anything out on policy path, via CNBC. Fed in good position because of strong labour market.No need to hurry to cut rates; the Fed could potentially even hike rates if inflation fails to come down further.

- Fed's Bowman (voter) would have supported either waiting to slow QT pace or more tapered slowing in balance sheet run-off, according to Reuters. 'In my view' bank reserves are not yet near 'ample' levels given the still-sizable take-up of ON-RRP. Important to keep reducing balance sheet size to reach ample reserves as soon as possible and while the economy is strong. Important to communicate any change to the run-off rate does not reflect a change in the Fed's monetary policy stance. 'Strongly' supports the principle of balance sheet holdings primarily being composed of Treasuries. A longer-run balance sheet 'tilted slightly' toward shorter maturities would allow flexibility in approach. In future, when the Fed conducts QE to restore market functioning or financial stability it should communicate that purchases will be temporary and unwound when market conditions have normalised. FOMC would have benefited from an earlier decision to taper and end QE in 2021; and would have allowed earlier rate hikes.

- Fed's Mester (voter) said would be preferable for FOMC statements to use more words to describe the current assessment of the economy and how that influences the outlook, as well as risks to that outlook, according to Reuters. Scenario analysis should also be incorporated as a standard part of Fed communications. Would like the Fed to publish an anonymised matrix of economic and policy projections so market participants can see the linkage between each participant’s outlook and their view of appropriate policy associated with that outlook. Expect the Fed will consider communications as part of its next monetary policy framework review.

- BoE Deputy Governor Broadbent rejected claims that the monetary policy committee acted too slowly and hit back at critics who have accused it of failing to control inflation, according to The Times.

- ECB’s Lane said keeping rates overly restrictive for too long could push inflation below target in the medium-term which would require corrective action that could even mean having to descend below neutral, while they think inflation over the coming months will bounce around at the current level and then will see another phase of disinflation bringing them back to the target later next year, according to Reuters. It was separately reported that ECB’s Lane said policymakers needed to keep rates in restrictive territory this year to ensure inflation kept easing, according to FT.

- ECB’s Rehn said inflation is converging to their 2% target in a sustained way and the time is thus ripe in June to ease the monetary policy stance and start cutting rates, while he added this assumes the disinflationary trend will continue and there will be no further setbacks in the geopolitical situation and energy prices.

- ECB’s Villeroy said they have significant room for rate cuts with the Deposit Facility rate at 4% and barring a surprise, a rate cut in June is a done deal, while Villeroy added that he doesn’t say they should commit already on July but they should keep their freedom on the timing and pace.

- ECB's Schnabel said QE could have weakened the transmission of monetary policy during the recent tightening cycle, according to Reuters.

- RBNZ activated debt-to-income restrictions which will create limits on the amount of high-DTI lending banks can make and will include an allowance for banks to do 20% of their lending outside of our specified limits, while banks must comply with new restrictions from July 1st.

- BoJ Monetary Affairs Department Director-General Masaki said changes in wages in real terms will move to positive territory on a Y/Y basis and need to keep an eye on energy prices and forex moves, according to Reuters.

APAC TRADE

- APAC stocks were mixed with price action mostly rangebound in the absence of a lead from Wall St and as geopolitical uncertainty lingered following an Israeli strike on Rafah which killed dozens of Palestinians on Sunday.

- ASX 200 swung between gains and losses albeit in a thin range with sentiment not helped by soft retail sales.

- Nikkei 225 retreated after stalling beneath the 39,000 level as participants also digested the firm Services PPI data which accelerated by its fastest pace since 2015.

- Hang Seng and Shanghai Comp were somewhat varied as Hong Kong outperformed with Alibaba Health Information Technology front-running the gains post-earnings, while there was also notable strength in China's major oil companies after the recent upside in underlying commodity prices. Conversely, the mainland lacks conviction with only brief support seen in property stocks following Shanghai's latest measures to spur the flagging sector.

NOTABLE ASIA-PAC HEADLINES

- China’s Politburo said preventing and defusing financial risks is linked to national security and people’s property security, while it added China must act to prevent and defuse financial risks, as well as promote high-quality financial development Furthermore, it stated financial risks are a major hurdle that must be overcome, according to state media.

- Shanghai adjusted the minimum down payment ratio for first-home buyers to no less than 20% and for second-home buyers to no less than 30%, while it cut the lower limit for interest rates on first-home mortgages to LPR minus 45bps. Furthermore, Shanghai is to establish and improve the housing system, explore buying housing through state-owned platform companies and other entities, as well as optimise the supply of housing security.

- Japanese Finance Minister Suzuki said it is important for currencies to move in a stable manner reflecting fundamentals. Suzuki added that a weak yen boosts exporters' profits but increases the burden for consumers, while he is concerned more about the negative impact of a weak yen and is closely watching FX moves.

- BoJ says its underlying inflation measure all fell below 2% in April.

- Chinese President Xi has urged promoting high-quality and sufficient employment, according to state media.

- China Politburo says China will promote the coordination and linkage of fiscal, monetary, investment, consumption, industrial, regional and other policies with employment policies, via state media.

DATA RECAP

- Japanese Services PPI YY (Apr) 2.8% vs Exp. 2.3% (Prev. 2.3%)

- Australian Retail Sales MM Final (Apr) 0.1% vs. Exp. 0.2% (Prev. -0.4%)