US Market Open: NQ outperforms post-Nvidia earnings, Bunds softer following German/EZ PMIs; Fed's Bostic due

23 May 2024, 11:10 by Newsquawk Desk

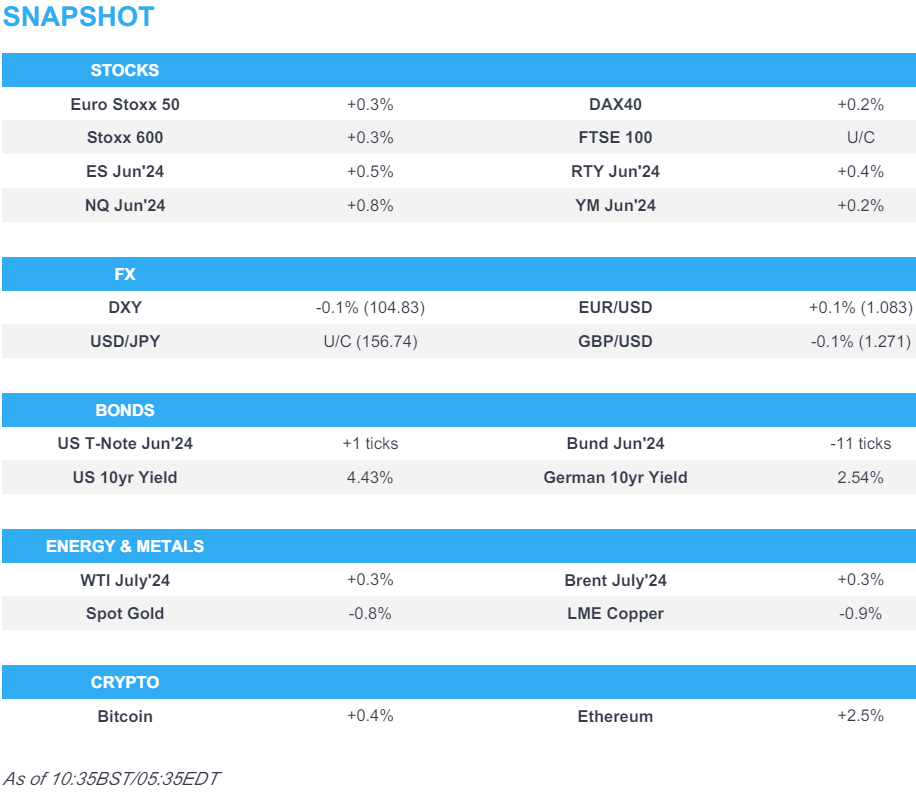

- European bourses are modestly firmer with Tech lifted by post-earning strength in Nvidia (+7% pre-market); NQ outperforms.

- Dollar is slightly softer, Kiwi continues the prior day’s gains, Euro was choppy on Flash PMIs but ultimately firmer and saw no reaction to higher Q1 wages.

- Treasuries are flat, whilst Bunds are softer following German/EZ PMIs ahead of US supply.

- Crude is firmer and near session highs, spot gold and copper futures aggressively pull back after printing record highs on Monday.

- Looking ahead, US PMIs, US IJC, Comments from BoE's Pill, ECB's Villeroy, and Fed’s Bostic, Supply from US. Earnings: Ralph Lauren, Medtronic & Intuit

EUROPEAN TRADE

EQUITIES

- European bourses (Stoxx 600 +0.2%) hold a modest upward bias, and overall unreactive to the mostly well-received EZ Flash PMI data.

- European sectors are mixed with no overarching bias. Tech outperforms following NVIDIA's blockbuster earnings and 10-for-1 stock split yesterday. Utilities are dragged lower by National Grid announcing a GBP 7bln rights issue.

- US Equity Futures (ES +0.5%, NQ +0.8%, YM Unch. RTY +0.2%) are mostly firmer but to varying degrees with the ES and NQ benefitting the most from NVIDIA's (+7% pre-market) blockbuster earnings yesterday.

- UBS expects Stoxx 600 year-end target to be 540 (currently 522)

- Click here and here for the sessions European pre-market equity newsflow.

- Click here for more details.

FX

- Dollar is broadly modestly softer vs. peers after running out of steam ahead of 105 (printing a high at 104.96). FOMC minutes were seen as hawkish, though with focus on the upcoming data releases.

- EUR/USD was initially knocked lower by disappointing French PMI metrics before a better outturn for Germany and (to an extent) EZ undid some of the damage. As it stands, EUR/USD is a touch firmer but shy of yesterday's 1.0863 best. There was limited follow through to Eurozone asset prices following the higher than expected Q1 wages release.

- GBP is softer and towards session lows following a miss on services and composite PMI metrics. Cable currently at 1.2710, and still yet to test 1.2700 to the downside (also yesterday's trough).

- JPY is flat vs. the USD after pulling back from its 156.89 peak overnight; highest level since 1st May; and currently sits around 156.70.

- NZD/USD once again the best performer across the majors in the wake of yesterday's RBNZ hawkish hold decision and despite less hawkish commentary from RBNZ's Orr.

- Click here for more details.

- Click here for NY Opex details.

FIXED INCOME

- USTs are contained with only limited spill-over selling seen in the wake of EZ PMI data with US metrics looming large later in the session; For now, the Jun'24 contract remains tucked within yesterday's 108.28+-109.08 range.

- Bunds initially spiked higher in wake of the French PMIs before it took a tumble lower on account of better-than-expected German PMI metrics which saw beats across all three metrics and the composite measure moving further into expansionary territory; much of the downside has been pared in recent trade. There was limited follow through to Eurozone asset prices following the higher than expected release.

- Gilts remain pressured in the wake of yesterday's hot inflation print and spill over selling from European paper, though was unreactive to the UK PMI metrics. Jun'24 contract had been as low as 96.58 before recovering modestly.

- Click here for more details.

COMMODITIES

- Crude prices were initially subdued though climbed higher following upbeat German Flash PMIs in which now forecasts "solid growth" for Germany. Brent near session highs and just above USD 82/bbl.

- Precious metals are lower across the board in a continuation of the price action seen since the surge after last weekend, with major geopolitical developments light, keeping risk premiums at bay; XAU fell from a USD 2,383.79.oz high to a USD 2,354.98/oz low.

- Base metals are sliding across the board, again in a continuation of the recent losses with 3M LME copper now around USD 10,250/t.

- Russian Energy Ministry said Russian oil production was within OPEC+ guidelines in Q1 and Russia exceeded OPEC+ quota in April due to technical reasons in output cuts, while it added that Russia is to submit a plan soon on compensation to the OPEC secretariat, according to Reuters.

- Click here for more details.

CRYPTO

- Bitcoin trades modesly fimer but remains under USD 70k while Ethereum continues to gain above USD 3.8k.

- US House voted to pass the FIT21 cryptocurrency regulations bill that creates a path for cryptocurrencies to be exempt from many securities regulations if they achieve a sufficient level of decentralisation.

NOTABLE DATA RECAP

- EZ HCOB Composite Flash PMI (May) 52.3 vs. Exp. 52.0 (Prev. 51.7); Services Flash PMI (May) 53.3 vs. Exp. 53.5 (Prev. 53.3); Manufacturing Flash PMI (May) 47.4 vs. Exp. 46.2 (Prev. 45.7).

- French HCOB Composite Flash PMI (May) 49.1 vs. Exp. 51.0 (Prev. 50.5); Services Flash PMI (May) 49.4 vs. Exp. 51.7 (Prev. 51.3); Manufacturing Flash PMI (May) 46.7 vs. Exp. 45.8 (Prev. 45.3); "Our HCOB Nowcast expects 0.3% economic growth for the second quarter down from 0.4%".

- German HCOB Composite Flash PMI (May) 52.2 vs. Exp. 51.0 (Prev. 50.6); Services Flash PMI (May) 53.9 vs. Exp. 53.5 (Prev. 53.2); Manufacturing Flash PMI (May) 45.4 vs. Exp. 43.1 (Prev. 42.5); Our GDP Nowcast estimates a 0.3% GDP increase in the second quarter compared to the first quarter".

- EZ Negotiated Wages (Q1): 4.69% (exp. 4.3%, prev. 4.45%)

- UK Flash Composite PMI (May) 52.8 vs. Exp. 54.0 (Prev. 54.1); Manufacturing PMI (May) 51.3 vs. Exp. 49.5 (Prev. 49.1); Services PMI (May) 52.9 vs. Exp. 54.7 (Prev. 55.0)

NOTABLE EUROPEAN HEADLINES

- Germany's DIHK expects German GDP to stagnate this year vs. prev. view of a 0.5% contraction; Inflation to fall to 2.3% in 2024 from 5.9%; Exports expected to stagnate this year; Private consumption to increase by 1% this year.

- IMF sees French GDP growth at 0.8% this year and 1.3% in 2025.

- ECB's de Guindos said a prudent approach would back a 25bp cut.

- HSBC and Deutsche Bank now expect the BoE to start cutting rates in August (vs prev. forecast of June).

NOTABLE US HEADLINES

- NVIDIA Corp (NVDA) Q1 2024 (USD): Adj. EPS 6.12 (exp. 5.57), Revenue 26.04bln (exp. 24.57bln); announced ten-for-one forward stock split and cash dividend raised 150% to USD 0.01/shr on a post-split basis.

- Tesla (TSLA) "broke ground" on megapack battery factory in Shanghai on Thursday, according to Chinese state media.

- 300 Boeing (BA) planes used by United (UAL) and American Airlines (AAL) have potentially fatal fault that could cause jets to explode, Daily Mail reports

GEOPOLITICS

CHINA-TAIWAN

- China's military began joint military drills surrounding Taiwan, according to Chinese state media.

- Chinese state broadcaster said Taiwan President Lai's May 20th speech was a 'complete confession' of Taiwan independence and seriously 'provoked' the One-China principle, as well as undermined peace and stability across the Taiwan Strait. China's state broadcaster stated that Lai's speech was 'extremely harmful' and used 'country' to refer to Taiwan throughout his speech, while Lai has no sincerity in promoting cross-strait exchanges and China's drills around Taiwan are 'punishment' for Lai's provocation.

- Taiwan Defence Ministry said it expresses strong condemnation of Chinese military drills and has dispatched forces, while it will take practical actions to protect freedom and democracy, as well as have the 'ability, determination and confidence to ensure national security'. Taiwan's Defence Ministry said ground forces have reinforced defence coordination and safety of military camps, while air defence and land-based missile forces are collecting intelligence on targets.

- Taiwan's Presidential Office said it is regrettable to see China threatening Taiwan's democratic freedoms and regional peace and stability with unilateral military provocation and Taiwan's consistent position is that maintaining regional peace and stability is the common responsibility and goal of both sides of the strait.

- Senior Taiwanese Security Official said around 30 Chinese military planes and a dozen military ships came close to Taiwan as of midday Thursday, some of which crossed the Taiwan Strait median line and approached close to areas of Taiwan contiguous zone

MIDDLE EAST

- US Defense Secretary Austin advocated during a call with Israeli Defence Minister Gallant for an effective mechanism to deconflict humanitarian and military operations in Gaza, according to the Pentagon.

RUSSIA

- Blasts were heard in Russia's Belgorod after missile attack warning, according to RIA.

APAC TRADE

- APAC stocks traded mixed after the negative performance of cash markets stateside and with US futures boosted after hours owing to Nvidia's earnings which also helped some semiconductor names in Asia.

- ASX 200 was dragged lower by underperformance in the mining sector after recent declines in underlying metal prices and with industry giant BHP pressured after Anglo American rejected its latest proposal and gave it another 7 days to make an improved offer.

- Nikkei 225 was underpinned and reclaimed the 39,000 status with the index helped by recent currency weakness and as tech stocks were inspired by Nvidia's strong earnings report.

- Hang Seng and Shanghai Comp were subdued amid ongoing frictions after the USTR posted details of the proposed tariffs on Chinese imports and China’s took countermeasures against a dozen US firms.

NOTABLE ASIA-PAC HEADLINES

- BoK kept its base rate unchanged at 3.50%, as expected, with the decision unanimous, while it stated that consumption recovery is modest and it will maintain a restrictive policy stance for a sufficient period of time. BoK said exports are to sustain growth and it is to monitor trends of slowing inflation and risks to financial stability. BoK Governor Rhee said chances of a policy interest rate increase are "limited" and that one board member said the path to a rate cut should be opened for the next three months, while Rhee added it is unclear when they will start discussing interest rate cuts given the uncertainty in inflation path and they have not discussed the size of cuts needed.

- South Korea announced a KRW 26tln support package for the chip industry and President Yoon announced they are to establish a KRW 17tln semiconductor financial assistance program at state-run Korea Development Bank, while they will extend the tax credit for the semiconductor industry set to expire at the end of this year.

- MAS said the current policy stance remains appropriate and the prevailing rate of the exchange policy band is needed to keep restraining imported inflation and domestic cost pressures.

- RBNZ Governor Orr said it is disappointing how stubborn domestic component inflation remains and the biggest risk we run is that we don't get inflation low and stable, according to Reuters. RBNZ Governor Orr also commented in a Bloomberg interview that another rate hike would only be meaningful if they believed inflation was getting away from them and noted that patience on inflation is not exhausted. Furthermore, he said inflation will not hinge on any single piece of data and that they can start to ease before inflation hits 2%.

DATA RECAP

- Japanese JibunBK Manufacturing PMI Flash SA (May) 50.5 (Prev. 49.6); Services PMI Flash SA (May) 53.6 (Prev. 54.3)

- Australian Judo Bank Manufacturing PMI Flash (May) 49.6 (Prev. 49.6); Judo Bank Services PMI Flash (May) 53.1 (Prev. 53.6)

- New Zealand Retail Sales Volumes QQ (Q1) 0.5% vs. Exp. -0.3% (Prev. -1.9%); Core Retail Sales QQ (Q1) 0.4% vs Exp. 0.0% (Prev. -1.7%)