US Market Open: Equities trade tentatively ahead of FOMC Minutes & NVDA earnings, Bonds subdued post-UK CPI

22 May 2024, 10:55 by Newsquawk Desk

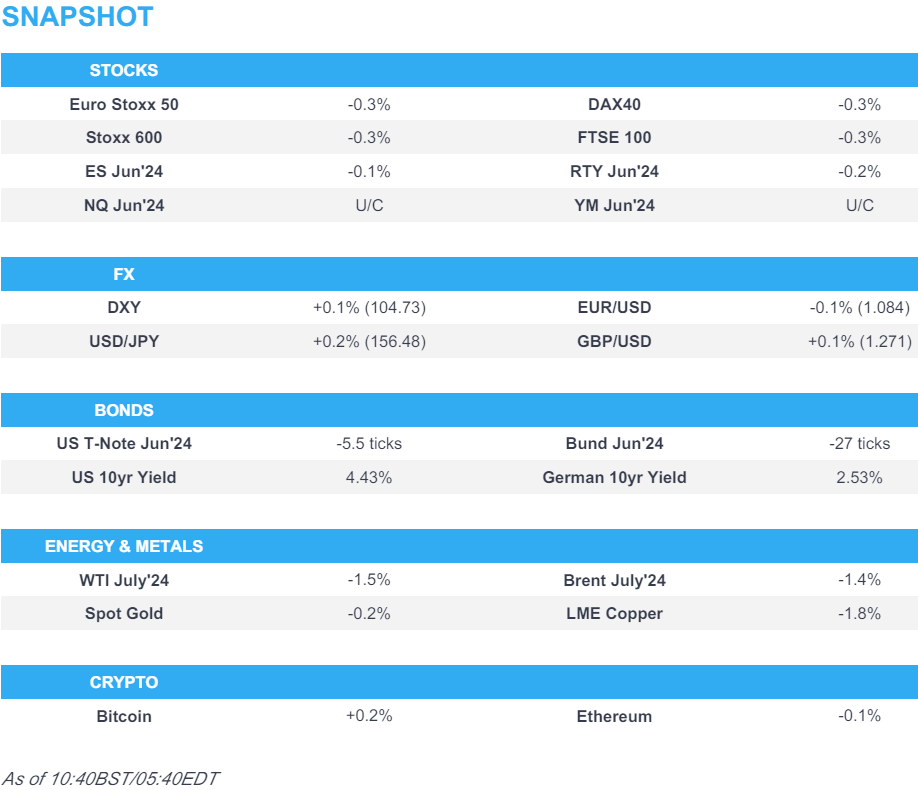

- European bourses are entirely in the red, whilst US futures trade tentatively ahead of FOMC Minutes and Nvidia earnings

- Dollar is incrementally firmer, Kiwi outperforms post-RBNZ & GBP bid on UK inflation metrics

- Bonds are lower after hotter-than-expected UK CPI metrics, with Gilts the clear underperformer

- Crude is subdued, XAU is softer alongside a broader pullback in base metals

- Looking ahead, Fed Minutes, Speak from Fed's Goolsbee, BoE’s Breeden, Supply from the US, Earnings from Nvidia, Analog Devices, TJX & Target

EUROPEAN TRADE

EQUITIES

- European bourses, (Stoxx 600 -0.3%), are subdued across the board, but within recent ranges as the tone from APAC reverberated into Europe.

- European sectors are mostly lower, with the breadth of the market fairly narrow; Autos are found at the foot of the pile, after EU car registrations showed a fall in EV market share. Energy is also hampered by broader weakness in the crude complex.

- US equity futures (ES -0.1%, NQ U/C, RTY -0.2%) are trading tentatively in a catalyst-thin session, with focus on the FOMC Minutes and after-market earnings from Nvidia.

- Click here and here for the sessions European pre-market equity newsflow.

- Click here for more details.

FX

- DXY is slightly firmer but is showing mixed performance vs. peers (softer vs. NZD and GBP but firmer vs. CHF and JPY). DXY has caught a recent bid and currently trades near session highs at 104.77.

- EUR is marginally softer vs the Dollar but a session of losses vs. the GBP; In terms of price action for EUR/USD, the pair is currently respecting yesterday's 1.0842-74 range.

- GBP is firmer in the wake of an unambiguously disappointing inflation report for the BoE. Y/Y measures fell from their priors but came in hotter-than-expected, as such the first full cut is now priced in November vs September pre-release. Accordingly, Cable vaulted to a high of 1.2761, though has since pared almost the entire move amid the recent Dollar strength, although EUR/GBP holds onto losses.

- Antipodeans are mixed vs. the USD with NZD the best performer across the majors post-RBNZ rate decision. The hawkish lean of the release saw NZD/USD spike higher to 0.6152. AUD/USD is a touch softer vs. the USD in quiet newsflow and as copper prices pull back.

- PBoC set USD/CNY mid-point at 7.1077 vs exp. 7.2376 (prev. 7.1069).

- Click here for more details.

- Click here for NY Opex details.

FIXED INCOME

- USTs are softer following the broader dynamics in fixed income markets but to a lesser extent than peers. Today's FOMC minutes will be parsed for details on what lies ahead for the Fed. Trough thus far at 108.31+ low matched that of yesterday's but failed to make any headway below that level.

- Gilts are notably lagging peers in the wake of the latest UK inflation release whereby Y/Y measures fell from their priors but came in hotter-than-expected. Gilts gapped lower by over a point, printing a low at 96.83, before stabilising on a 97 handle.

- Bunds were already on the backfoot before subsequently being dragged lower by UK inflation metrics. Jun'24 Bund contract went as low as 130.30, tripping below yesterday's trough at 130.53.

- UK sells GBP 4bln 4.125% 2029 Gilt: b/c 3.2x (prev. 3.21x), average yield 4.199% (prev. 4.251%), tail 0.6bps (prev. 0.8bps).

- Germany sells EUR 3.283bln vs exp. EUR 4bln 2.20% 2034 Bund: b/c 2.8x (prev. 2.5x), average yield 2.53% (prev. 2.54%) & retention 17.9% (prev. 19.03%)

- Click here for more details.

COMMODITIES

- Crude is lower in a continuation of the recent trend, with prices also pressured by the surprise build in private inventories (Crude +2.5mln vs exp. -2.5mln) ahead of today's DoEs; Brent July closer to the bottom end of a 81.57-82.63/bbl parameter.

- Precious metals are softer with spot gold subdued amid a lack of notable geopolitical developments in recent days and ahead of FOMC minutes; XAU resides within a USD 2,410.69-2,426.62/oz range.

- A pullback is seen across most base metals following the recent rally, with profit-taking not to be discounted, with 3M LME copper towards the bottom end of a 10,636.50-10,857.50 intraday parameter

- Global crude steel output -5.0% Y/Y; Chinse crude steel output -7.2% Y/Y

- Norway's April Prelim oil production 1.854mln BPD (vs 1.84mln BPD in March), gas output 10.4bcm (vs 364.5mcm/day in March), according to the Oil Directorate

- China's Coal Group said that China's May coal imports are likely to be lower than April's 42.5mln metric tons

- US Private Energy Inventory Data (bbls): Crude +2.5mln (exp. -2.5mln), Cushing +1.8mln, Gasoline +2.1mln (exp. -0.7mln), Distillate -0.3mln (exp. -0.4mln).

- Commerzbank said it expects Gold price to fall to USD 2300/toz in H2'24; raises forecast for Silver to USD 30/toz (prev. USD 29)

- Click here for more details.

CRYPTO

- Bitcoin has stabilised just beneath USD 70k, with Ethereum holding just above USD 3.7k.

NOTABLE DATA RECAP

- UK CPI YY (Apr) 2.3% vs. Exp. 2.1% (Prev. 3.2%); CPI MM (Apr) 0.3% vs. Exp. 0.2% (Prev. 0.6%); Core CPI MM (Apr) 0.9% vs. Exp. 0.7% (Prev. 0.6%); Core CPI YY (Apr) 3.9% vs. Exp. 3.6% (Prev. 4.2%)

- UK CPI Services YY (Apr) 5.90% vs. Exp. 5.50% (Prev. 6.00%; vs BoE forecast 5.50%); CPI Services MM (Apr) 1.50% vs. Exp. 1.10% (Prev. 0.60%)

- UK PPI Input Prices MM NSA (Apr) 0.6% vs. Exp. 0.7% (Prev. -0.1%, Rev. -0.2%); YY NSA (Apr) -1.6% vs. Exp. -1.2% (Prev. -2.5%)

- UK PSNB Ex Banks GBP (Apr) 20.514B GB vs. Exp. 19.3B GB (Prev. 11.939B GB, Rev. 13.063B GB)

OTHER DATA

- Swedish Unemployment Rate (Apr) 8.9% (Prev. 9.2%)

- South African CPI MM (Apr) 0.3% vs. Exp. 0.4% (Prev. 0.8%); YY (Apr) 5.2% vs. Exp. 5.3% (Prev. 5.3%)

NOTABLE EUROPEAN HEADLINES

- EU New car registrations: +13.7% in April 2024; battery electric 11.9% market share (vs 13% in March), according to acea. EU New Car Registrations by company in April Y/Y: Volkswagen (VOW3 GY) +15.5%. Stellantis (STLAP FP/ STLAM IM) +1.7%. Renault (RNO FP) +11.0%. BMW (BMW GY) +11.5%. Mercedes-Benz (MBG GY) +4.2%. Toyota (7203 JT) +47.3%. Nissan (7201 JT) +14.3%. Ford (F) -9.1%. Tesla (TSLA) +3.0%.

- UK ONS House Price Index (Mar) +1.8% (vs -0.2% in Feb).

- Barclays removed its expectations that the BoE will conduct the first rate cut in June.

NOTABLE US HEADLINES

- Fed's Mester (voter) said expect above-trend growth for the year and keeping rates restrictive is not that big of a risk right now given job market strength. Mester said she raised her estimate of the long-run neutral rate in the last projection and the current level of policy may not be "as restrictive" as it might otherwise have been, while she needs to see a few more months of inflation coming down and is also watching expectations.

- Fed's Collins (non-voter) said elevated uncertainty continues to be a feature of the economy and cannot overreact to any data point, while she added this is a period when patience really matters and uncertainty is a key factor at this point. Furthermore, she said there are a lot of reasons to think Fed policy is "moderately" restrictive with some impacts still in the pipeline and the neutral rate may be higher at least in the medium term.

GEOPOLITICS

MIDDLE EAST

- US senior official said negotiators are nearing a final set of arrangements for the US-Saudi defence deal and it is 'pretty much there to do’, while the deal includes a security component and nuclear agreement but the deal is not done and requires more work. The official said elements such as a credible pathway to Palestinian statehood still have to be completed, while the US talked with Israeli officials and reinforced President Biden's concerns about a Rafah ground invasion. Furthermore, the official said they had a very detailed discussion with Israelis about how to transition to a stabilisation phase in Gaza.

OTHER

- China's Foreign Minister Wang said in talks with Iran's Deputy Foreign Minister that China will continue to strengthen strategic cooperation with Iran, safeguard common interests, and make endeavours for regional and world peace, according to Reuters.

- Russian Foreign Ministry said Russia's response will not only be political if France sends troops to Ukraine, according to RIA.

- Russian Defence Ministry proposed to change external border of Russian territorial waters in Baltic Sea, via Interfax citing draft bill

APAC TRADE

- APAC stocks were mostly rangebound as global markets brace for the FOMC Minutes and Nvidia earnings.

- ASX 200 just about kept afloat as strength in the heavy industries picked up the slack from the sluggish consumer and tech sectors.

- Nikkei 225 underperformed following a retreat beneath the 39,000 level and amid mixed data releases as trade data disappointed but machinery orders topped forecasts and showed a surprise M/M expansion.

- Hang Seng and Shanghai Comp were somewhat varied as the former mildly resumed its advances with XPeng among the notable gainers in Hong Kong due to its Q2 delivery guidance, while the mainland was contained amid a lack of drivers and lingering trade frictions.

NOTABLE ASIA-PAC HEADLINES

- RBNZ kept the OCR unchanged at 5.50% as expected, while it noted that monetary policy needs to be restricted and it raised its OCR projections with the OCR seen at 5.61% in September 2024 (prev. 5.60%), 5.54% in June 2025 (prev. 5.33%), 5.40% in September 2025 (prev. 5.15%) and at 2.99% in June 2027. RBNZ said restrictive monetary policy has reduced capacity pressures in the New Zealand economy and lowered consumer price inflation, as well as noted that annual consumer price inflation is expected to return to within the committee's 1%-3% target range by the end of 2024. RBNZ Minutes noted the committee agreed that interest rates need to remain at a restrictive level for a sustained period to ensure annual headline CPI inflation returns to the 1%-3% target range, while the committee agreed that interest rates may have to remain at a restrictive level for longer than anticipated in the February Monetary Policy Statement to ensure the inflation target is met. Furthermore, the committee discussed the possibility of increasing the OCR at this meeting.

- RBNZ Governor Orr said during the press conference that it would take time for domestic inflation to decline, while he added the economy has a lower potential growth rate and he is unsure if that is temporary. Orr also commented that they have limited upside room for inflation surprises and the OCR track is a central projection not an absolute prediction, as well as noted that they had a real consideration on raising rates at this meeting.

DATA RECAP

- Japanese Trade Balance (JPY)(Apr) -462.5B vs. Exp. -339.5B (Prev. 387.0B)

- Japanese Exports YY (Apr) 8.3% vs. Exp. 11.1% (Prev. 7.3%)

- Japanese Imports YY (Apr) 8.3% vs. Exp. 9.0% (Prev. -5.1%)

- Japanese Machinery Orders MM (Mar) 2.9% vs. Exp. -2.2% (Prev. 7.7%)

- Japanese Machinery Orders YY (Mar) 2.7% vs. Exp. 2.3% (Prev. -1.8%)