US Market Open: Strong Big Tech earnings prop up equities, JPY lower post-BoJ & Dollar flat ahead of US PCE

26 Apr 2024, 11:20 by Newsquawk Desk

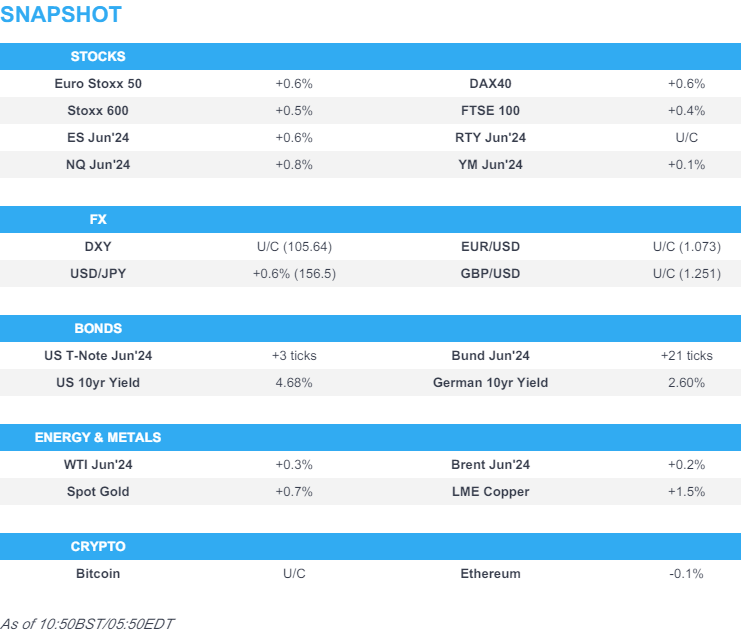

- Equities are firmer, benefiting from strong Big Tech earnings; Google (+11.7%), Microsoft (+3.6%)

- Dollar is flat, USD/JPY moved lower in quick succession before paring back, Aussie outperforms given the risk tone and higher metal prices

- Bonds are modestly firmer, though very much contained ahead of US PCE

- Crude within recent ranges, XAU trudges higher and base metals entirely in the green; 3M LME topped USD 10,000/t

- Looking ahead, US PCE, Personal Income, Earnings from Colgate, Exxon, Chevron & Phillips 66.

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx 600 (+0.5%) are entirely in the green, though trade has been contained at session highs, as participants await March's US PCE at 13:30 BST.

- European sectors are almost entirely in the green, with the exception of Chemicals, following poor IMCD (-9.1%) results. Tech tops the pile, with optimism lifted following strong large-cap Tech earnings in the US.

- US Equity Futures (ES +0.7%, NQ +0.9%, RTY +0.1%) are entirely in the green, with the NQ outperforming, benefitting from significant pre-market strength in both Google (+11.1%) and Microsoft (+3.6%), after reporting strong earnings after-market.

- Click here and here for the sessions European pre-market equity newsflow.

- Click here for more details.

FX

- USD is around flat, and holding within a 105.40-71 range. USD was initially being propped up by JPY softness post-BoJ, although that has abated somewhat, amid Yen intervention speculation.

- JPY is the clear laggard across the majors following the BoJ policy announcement overnight, which provided no hawkish surprise. USD/JPY took another leg higher amid BoJ Ueda's press conference, before being slapped down to sub-155 levels, a few hours later. Some will likely view the move as intervention but we are yet to see any official confirmation of this.

- EUR is flat vs. the USD and breached yesterday's 1.0740 best. If the pair ventures higher, 1.0756 from April 11th is the next potential target.

- Antipodeans are firmer vs. the USD and outmuscling peers alongside the favourable risk environment. AUD/USD has gained a firmer footing above its 200 and 50DMAs at 0.6526 and 0.6532 respectively with focus now on a potential approach of 0.66

- PBoC set USD/CNY mid-point at 7.1056 vs exp. 7.2449 (prev. 7.1058).

- Click here for more details.

FIXED INCOME

- USTs are a touch firmer after yesterday's data induced losses, which sent the Jun'24 UST to a contract low of 107.04. Today's trade has been contained within a 107.04-108.01 range, with all eyes on March's US PCE metrics later.

- Bund price action has been following USTs and attempting to recoup recently lost ground which has been inspired this week by a combination of better data and speak from hawkish ECB members. Bunds are so far respecting yesterday's 129.53-130.38 range.

- Gilts are firmer and in-fitting with global peers in an attempt to claw back recent losses. However, with a lack of UK-specific drivers, UK paper will likely remain at the whim of global peers.

- Click here for more details.

COMMODITIES

- A relatively tame session thus far for the crude complex following Thursday's choppy trade, as participants await monthly US PCE metrics; Brent Jun'24 range between 89.08-69/bbl.

- Precious metals are firmer amid the softer Dollar and ahead of the US PCE data, with spot silver narrowly leading vs spot gold. XAU topped yesterday's peak (USD 2,344.93/oz) to trade in a current intraday range between USD 2,326.36-2,352.30/oz.

- Base metals are stronger across the board amid bullish momentum after copper crossed key levels, with the broader complex underpinned by the softer Dollar and broader risk appetite; 3M LME copper is posting gains of over USD 100/t at the time of writing after mounting the key USD 10,000/t mark to levels last seen in 2022.

- India Oil Minister said cartel of oil producers are responsible for current volatility in the market; oil producers are cutting down and holding back production, according to ETNow.

- Click here for more details.

NOTABLE EUROPEAN HEADLINES

- ECB's Panetta said they must weigh the risk of monetary policy becoming too tight, while he added that timely and small rate cuts would counter weak demand and could be paused. Furthermore, he stated that hesitations in adjusting rates would hurt investment and productivity, while large rate cuts could create a credibility issue.

- ECB Consumer Inflation Expectations survey (Mar) - 12-months ahead 3.0% (prev. 3.1%); 3-year ahead 2.5% (prev. 2.5%). Economic growth expectations for the next 12 months 1.1% (prev. -1.1%)

- SNB Chair Jordan said SNB has been successful in fight against inflation; uncertainty remains elevated and shocks can occur at and time

DATA RECAP

- UK GfK Consumer Confidence (Apr) -19.0 vs. Exp. -20.0 (Prev. -21.0)

- Spanish Retail Sales YY (Mar) 0.6% (Prev. 1.9%); Unemployment Rate (Q1) 12.29% (Prev. 11.76%, Rev. 11.80%)

- EU Money-M3 Annual Growth (Mar) 0.9% vs. Exp. 0.6% (Prev. 0.4%); Loans to Non-Fin (Mar) 0.4% (Prev. 0.4%); Loans to Households (Mar) 0.2% (Prev. 0.3%)

NOTABLE US HEADLINES

- US Secretary of State Blinken is to meet Chinese President Xi in Beijing on Friday 26th April, according to the US State Department.

EARNINGS

- Alphabet Inc (GOOGL) Q1 2024 (USD): EPS 1.89 (exp. 1.51), Revenue 80.54bln (exp. 78.59bln); board authorised Co. to repurchase up to an additional 70bln and declared a cash dividend of 0.20/shr. Shares +11.5% in pre-market trade

- Microsoft Corp (MSFT) Q3 2024 (USD): EPS 2.94 (exp. 2.82), Revenue 61.86bln (exp. 60.8bln). Shares +4.1% in pre-market trade

- Intel Corp (INTC) Q1 2024 (USD): Adj. EPS 0.18 (exp. 0.14), Revenue 12.70bln (exp. 12.78bln). Shares -7.5% in pre-market trade

- Snap Inc (SNAP) Q1 2024 (USD): Adj. EPS 0.03 (exp. -0.05), Revenue 1.19bln (exp. 1.12bln). Shares +23.5% in pre-market trade

- TotalEnergies (TTE FP) Q1 (USD): Adj. Net 5.11bln (exp. 5bln). Adj. EBITDA 11.5bln (exp. 11.1bln). Plans a USD 2bln share buyback Q2; Cash flow from operating activities 2.2bln (prev. 5.1bln Y/Y); Dividend +7% Y/Y

- Airbus (AIR FP) Q1 24 (USD): Adj. EBIT 600mln (exp. 789mln), Revenue 12.80bln (exp. 12.87bln), Gross Orders 170 (prev. 156), Net Orders 170 (prev. 142), Deliveries 142. Reaffirms 2024 guidance.

GEOPOLITICS

MIDDLE EAST

- "US Secretary of State Blinken to visit Israel on Tuesday", according to Sky News Arabia

- Hezbollah said it shelled an Israeli force with artillery at the site of Al-Malikiyah and achieved a direct hit, according to Al Jazeera.

OTHER

- US official said the US could announce as soon as Friday USD 6bln in new weapon purchases for Ukraine.

- North Korean leader Kim supervised the test-firing of multiple launch rockets, according to KCNA.

- China's Defence Ministry said Chinese and French militaries established a dialogue mechanism for cooperation between theatre commands, according to Reuters.

CRYPTO

- Bitcoin traded indecisively with price action on both sides of the USD 64,500 level.

APAC TRADE

- APAC stocks were mostly higher as the region digested recent market themes including disappointing US data, strong big tech earnings and the BoJ policy announcement.

- ASX 200 underperformed after the prior day's losses caught up with the index on return from holiday.

- Nikkei 225 was initially choppy and briefly dipped into negative territory as participants braced for the BoJ policy announcement and whether the central bank flags a reduction in bond buying, but then surged as the central bank kept policy settings unchanged and refrained from any major hawkish surprises.

- Hang Seng and Shanghai Comp. were underpinned by strength in tech and property, while the constructive mood was also facilitated by a meeting between US Secretary of State Blinken and Chinese Foreign Minister Wang where it was stated that the US-China relationship has stabilised although negative factors are building.

BoJ

- BoJ kept its policy settings unchanged with the short-term interest rate target at 0.0%-0.1%, as expected, with the decision made unanimously, while it dropped the reference from the statement that it currently buys about JPY 6tln worth of JGBs per month but stated that it will conduct JGB, commercial paper and corporate bond buying in line with the decision in March. BoJ said it must be vigilant to FX and market moves and their impact on the economy and prices but noted no excessive behaviour is seen in Japan's asset market and financial institutions' practices. Furthermore, it stated that if trend inflation rises, the BoJ will likely adjust the degree of monetary easing but also added to expect accommodative monetary conditions to continue for the time being. In terms of the latest Outlook Report, Board Members' Real GDP median forecast for Fiscal 2024 was cut to 0.8% from 1.2% but the Fiscal 2025 median forecast was maintained at 1.0%, while the Core CPI Fiscal 2024 median forecast was raised to 2.8% from 2.4% and Fiscal 2025 median forecast was raised to 1.9% from 1.8%.

- PRESS CONFERENCE: BoJ Governor Ueda said easy financial conditions will be maintained for the time being; Weak JPY so far is not having a big impact on trend inflation. Difficult to gauge timing of future rate hikes. Weak JPY so far is not having a big impact on trend inflation. Reduction in JGB buying in the future is in sight. Will not comment on FX moves. Click here for full comments.

NOTABLE ASIA-PAC HEADLINES

- Chinese Foreign Minister Wang said in a meeting with US Secretary of State Blinken that the China-US relationship has stabilised but negative factors are building, while he added that sliding into conflict with the US would be a lose-lose situation that they ask the US not to interfere with China's internal affairs. Furthermore, Blinken said there is no substitute for face-to-face diplomacy and they need to avoid miscalculations, while he hopes the US and China can make progress on agreements, citing fentanyl, military-to-military ties and AI risks.

- US is pushing allies in Europe and Asia to tighten restrictions on exports of chip-related technology and tools to China amid rising concerns about Huawei's development of advanced semiconductors, according to FT sources. US wants Japan, South Korea, and the Netherlands to use existing export controls more aggressively, including stopping engineers from their countries servicing chipmaking tools at fabs in China.

- ByteDance reportedly prefers shutting down the app rather than a sale if it exhausts all legal options and the algorithms TikTok relies on are deemed core to ByteDance’s overall operations, making the sale of the app unlikely, according to Reuters sources.

APAC DATA RECAP

- Tokyo CPI YY (Apr) 1.8% vs. Exp. 2.6% (Prev. 2.6%); CPI Ex. Fresh Food YY (Apr) 1.6% vs. Exp. 2.2% (Prev. 2.4%); CPI Ex. Fresh Food & Energy YY (Apr) 1.8% vs. Exp. 2.7% (Prev. 2.9%)